Sunday, January 28, 2024

Advancing Time: Economic Transition Should Be A Natural Progression

Advancing Time: Economic Transition Should Be A Natural Progression: In the Beginning, Everything Is New Economic transition should be a natural progression less altered by government intervention. This ...

Economic Transition Should Be A Natural Progression

|

| In the Beginning, Everything Is New |

Economic transition should be a natural progression less altered by government intervention. This thought is reinforced by the history of government intervention which reveals the failings of government to be efficient. I had to go deep into the archives of AdvancingTime to find this piece. It looks at the natural transition and progression in the economy that takes place when allowed. It is important to revisit this concept of economic evolution to understand what may be the best path forward.

The goal of this updated piece is to focus on how we might view a

developed country versus one that is in its early stages of economic

development. To do this, it might be helpful to think of a country in the early

stages of development as a newly planned development on the edge of

town. In the early stages of development, a great deal of money is spent

on building the infrastructure necessary for the planned community,

this includes roads, bridges, utility lines, and moving dirt. All this

may go on for many years as homes and commercial buildings are

constructed, all this creates jobs and new investment opportunities.

|

| At Some Point, Focus Moves Towards Repair And Restore |

At a certain stage of development, we reach a tipping point and a change takes place in the nature of how we spend our resources. As developments mature over time a larger percentage of outlays are spent on things like maintenance, updating, and upgrading existing buildings and infrastructure as needed, windows and roofs weathered by nature are replaced and parking lots are repaved and sealed. Rather than pouring money into strictly new construction, we find as an economy matures its rhythm changes and the focus should become sustaining what has been created to maximize our prior investment and extend its use.

An example of the natural transition that takes place over time is how during the early 1900s just after the automobile became popular among the masses garages began to appear in cities. These replaced the structures built for horses. In the neighborhoods being built at the time garages were constructed for one car and fairly narrow to accommodate the cars of the time. When cars became larger and families started owning more than one automobile these garages were no longer adequate and had to be enlarged. This example is used to highlight the fact that as lifestyles change neighborhoods change and evolve to better fit our needs and desires.

Over time with each new invention, we alter our homes and the economy as well as a way of adapting to the new realities life fosters upon us. In a perfect world, we would see developed areas not only continue to be maintained but steadily evolve and move forward. Construction tends to reflect the lifestyles of those living during the planning and building phase. Rather than bulldozing these buildings, I contend it would often be better to upgrade and preserve the best characteristics unique to the era in which buildings were conceived and do so in a way that makes economic sense. When it comes to buildings this means things such as adding insulation, replacing windows, or upgrading electrical panels.

Much of mankind has adopted mantras such as "move forward or die" and

"newer is better." These often repeated sayings tend to be short-sighted and discount

what those before us have brought to the table. Failure to recognize

this economic transition and reflect upon the natural progression of

society ushers in conflicts and even war. Part of this comes from shortsighted politicians trying to produce the ever-growing growth we have been told the majority of voters want. This

shortsightedness helps to explain why here in America we never hear

politicians on the national scene call for conservation unless it is

during an emergency. Consumers conserving, reducing waste, and any talk

of government austerity usually conflicts with the goals of lobbyists

hell-bent on creating growth at any cost.

|

| War Is Wasteful And Disrupts The Natural Progression |

The idea that the way to grow is to increase our population is flawed.

Simply adding mouths to feed and efforts to merely add new workers to

replace those retiring creates additional demand but is flawed and

shortsighted and ignores many other problems. Just getting bigger is not always better and we

must recognize even trees do not grow to the sky. At some point, we

must face reality. War is often the byproduct of such growth and war has

proven to be a poor answer to creating a better world. The bottom-line

is we should focus on a transition toward a future that is sustainable

over the long term.

When it comes to the economy, the pathway of natural transition means

finding new ways to manufacture and deliver goods. Unfortunately, the

shift from a growth economy to one that is sustainable over time is very

difficult to make for many countries. Change can create a slew of social

as well as economic problems. Sadly, we find that today the trend, often driven by governments trying

to stimulate growth, has become to encourage a total remove and replace. This

is seen in the way new regulations make things obsolete.

While ending the life of structures and systems prematurely may create jobs it also creates a lot of waste. Such waste is not new. We witnessed a huge amount of waste years ago when America rapidly switched its broadcast system from analog to digital, and hundreds of televisions were dumped into landfills. It seems that today this is again happening as we are pushed into electric vehicles.

The world of tomorrow will create many new challenges as automation reduces the need for workers. This will cause us to struggle with creating jobs that make people feel useful and create lives that have a purpose. The toxic mix of big predatory companies and big government interrupts the natural transition and overpowers individual choice.

When discussing such things it is easy to extend the conversation to things like income inequality and even more interesting issues. Such as, what do people deserve from society merely because they are born? Do individuals have an obligation to give back to society and not simply take and make demands upon it? These are questions we will continue to grapple with going forward and most likely the correct answer is embedded in reflection and thought.

(Republishing this article welcomed with reference to Bruce Wilds/AdvancingTime Blog)

Wednesday, January 17, 2024

Advancing Time: Stimulus Can Flow From Monetary Or Fiscal Policy

Advancing Time: Stimulus Can Flow From Monetary Or Fiscal Policy: Since 1982 whenever the economy has gotten into trouble the Fed has cut rates, often hard and fast. This has created a huge reliance on mone...

Stimulus Can Flow From Monetary Or Fiscal Policy

The other way to kick the economy to a higher level is through government spending or fiscal stimulus. This is also known as government money printing. The national deficit has exploded in the last fifteen years which indicates both types of policies are being overused. Unfortunately, expanding government fiscal policy often results in money being poorly spent, or flat out wasted, while leading to high government deficits.

This comes across as a MMT answer to economic growth which potentially leads to high inflation. An ugly often discounted fact is that it also results in a "bigger" government with a larger footprint. To be clear, since the beginning of 2022, spending on manufacturing construction has soared. It is difficult to tell when this government fiscal spending will run out of juice and slow. Much of this construction is due to a combination of companies re-shoring supply chains as well as government spending.

When the spending from government fiscal policy slows the economy will most likely also slow. This is especially true if the new manufacturing plants are highly automated and do not create a lot of new jobs. Another factor we face is the cost of products flowing from them may also be higher than those America had been importing from low-cost countries.

These policies are two distinctly different animals. It is important to remember that the growth generated from low-interest rates also has some drawbacks. This takes us to the issue of where is the stimulus coming from. It is very likely that stimulating the economy through monetary policy and stimulus from fiscal spending have different long-term implications for inflation.

Inflation, disinflation, and deflation are often misunderstood terms and so are the reasons driving them. Part of this comes from the confusion generated by government numbers versus real inflation. Real yields matter, and the government uses a method that tends to promote lower inflation figures or underestimate what we really face. It is only over the long term we can see how different and how bad these trends have become.

Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Thursday, January 11, 2024

Advancing Time: "It Will All End Badly" This All Points To A Massi...

Advancing Time: "It Will All End Badly" This All Points To A Massi...: While the economy and financial system chug forward, the idea we have charted a course that will end in ruin remains. Looking down the road ...

"It Will All End Badly" This All Points To A Massive Reset

Recognized for his wisdom and

achievements in economics, Meltzer was a professor of

political economy at Carnegie Mellon University and a visiting fellow at

the Hoover Institution. He authored the three-volume “A History of the

Federal Reserve” and for over 25 years he chaired the Shadow Open Market

Committee, a group that meets regularly to discuss the policy of the

Federal Reserve.

|

| Allen Meltzer On YouTube (click to start) |

To say Meltzer was not a fan of the economic policies that unfolded since 2008 is an understatement. “We’re

in the biggest mess we’ve been in since the 1930s,” he was quoted as saying, before he went on to claim that, “We’ve

never had a more problematic future.”

In a Wall Street Journal opinion piece on June 30, 2010, titled

"Why Obamanomics Has Failed" Meltzer wrote about some of the biggest enemies facing future

economic growth. He went on to say that the

administration's stimulus program failed. Two overreaching reasons explain the failure of

Obamanomics. First,

administration economists and their outside supporters neglected the

longer-term costs and consequences of their actions. Second, the

administration and Congress have through their deeds and words

heightened uncertainty about the economic future.

A few years later, in May of 2014, Allen Meltzer penned a piece that appeared in the Wall Street Journal. His opinion was highly valued, not only because it is based on his long-developed work and studies, but because of his age, he had far less motivation to lie than many of those currently involved in forming policies today. In the article, which is copied below, Meltzer gave his take on where the economy was headed. The fact he died in 2017 does not lessen his insight. Meltzer wrote;

The U.S. Department of Agriculture forecasts that food prices will rise as much as 3.5% this year, the biggest annual increase in three years. Over the past 12 months from March, the consumer-price index increased 1.5% before seasonal adjustment. These are warnings. Never in history has a country that financed big budget deficits with large amounts of central-bank money avoided inflation. Yet the U.S. has been printing money—and in a reckless fashion—for years.

The Obama administration has run huge budget deficits every year, which, together with the Bush administration, amounted to $6.7 trillion from 2006 to 2013. The Federal Reserve financed almost $3 trillion of these deficits by purchasing Treasury bonds and notes. The Fed has also purchased massive amounts of mortgage-backed securities. Today, with more than $2.5 trillion of idle reserves on bank balance sheets, there is enormous fuel for greater inflation once lending and money growth rise.

To avoid the kind of damaging inflation the U.S. experienced in the 1970s and early '80s, the Fed could raise interest rates, including the interest it pays banks on reserves, inducing banks to hold most of the $2.5 trillion of reserves idle. But interest rates high enough to discourage borrowing and lending would likely send the economy into another damaging recession.

Fed Chairwoman Janet Yellen recently admitted that the central bank doesn't have a good model of inflation. It relies on the Phillips Curve, which charts what economist Alban William Phillips in the late 1950s saw as a tendency for inflation to rise when unemployment is low and to fall when unemployment is high. Two of the most successful Fed chairmen, Paul Volcker and Alan Greenspan, considered the Phillips Curve unreliable. The Fed's forecasts of inflation ignore Milton Friedman's dictum that "inflation is always and everywhere" a result of excessive money growth relative to the growth of real output.

The Fed focuses far too much attention on distracting monthly and quarterly data while ignoring the longer-term effects of money growth. The country's present dilemma originated in 2008 when the Fed properly and forcefully prevented a collapse of the payments system. But long before idle reserves reached $2.5 trillion, the Fed didn't ask itself: What can we do by adding more reserves that banks cannot do by using their massive idle reserves? The fact that the reserves sat idle to earn one-quarter of a percent a year should have been a clear signal that banks didn't see demand to borrow by prudent borrowers.

The Fed's unprecedented quantitative easing since 2008 failed to lead to a robust recovery. The unemployment rate has gradually declined, but the main reason is that workers have withdrawn from the labor force. The stock market boomed, bringing support from traders, but the rise in asset prices of equities didn't stimulate growth by inducing investment in new capital. Investment continues to be sluggish.

And some side effects of the Fed policies have had ugly consequences. One of the worst is that ultra-low interest rates induced retired citizens to take substantially greater risks than the bank CDs that many of them relied on in the past. Decisions of this kind end in tears. Another is the loss that bondholders cannot avoid when interest rates rise, as they have started to do.

Accumulating data from the sluggish loan market and the weak responses of employment and investment should have alerted the Fed that the growth of reserves and the low interest rates haven't been achieving much. Similarly, the Fed should have noticed in recent years that instead of a strong housing-market recovery, not many individuals were taking out first mortgages. Many of the sales were to real-estate speculators who financed their purchases without mortgages and are now renting the houses, planning to resell them later.

Most of all the Fed years ago should have recognized that the country's economic problems weren't arising from monetary factors. Instead of keeping interest rates low to finance deficits, the Fed should have explained that costly regulation, increased health-care costs, wasteful spending, and repeated threats to raise tax rates were holding back the recovery.

Broadly speaking, the Obama administration has pursued a course the opposite of that taken by the Kennedy and Johnson administrations in the 1960s (and the Reagan administration in the 1980s). Kennedy-Johnson enacted across-the-board tax cuts: Promoting growth came first, redistribution later. By putting redistribution first and sacrificing growth, the Obama administration got neither. Ironically, despite often repeated demands for increased redistribution to favor middle- and lower-income groups, the policies pursued by the Obama administration and supported by the Federal Reserve have accomplished the opposite.

When the president campaigns in the midterm election, he will talk about the relative gains by the 1%. Voters should recognize that goosing the stock market through very low interest rates, not to mention the subsidies and handouts to cronies, have contributed to that result. We are now left with the overhang. Inflation is in our future. Food prices are leading off, as they did in the mid-1960s before the "stagflation" of the 1970s. Other prices will follow.

The point of this post is to clarify that just because we have muddled along putting band-aids on our economy does not mean that we have accomplished a great deal. The Trump economy was a continuation of deficit spending and the Biden economy has been even worse. Both have postponed the day of reckoning but most likely made it far worse. Allen Meltzer was a true old-school economist who understood this.The time the Federal Reserve bought for the country to come to terms with its many problems post-2008 has been squandered at a great cost. While many people claim the American economy was great before covid-19 hit, others like me who work on Main Street beg to differ. For years, an ugly reality has been masked by easy money and deficit spending.

Rather than being trapped in the here and now, economists might be wise

to reflect more on history. We can learn much from the failings of those

who lived before us. If Meltzer was still with us it is very likely he

would be appalled at the state of things today.While it is difficult to time when our false economy will

finally give up the ghost, it is clear this will all end badly. Today, the biggest question before us is when.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Monday, January 8, 2024

Advancing Time: Defined Pension Plans Have Put Many Workers At Risk

Advancing Time: Defined Pension Plans Have Put Many Workers At Risk: Over the years, we have seen a tremendous shift in risk from companies offering pensions to workers in the private sector. According to the ...

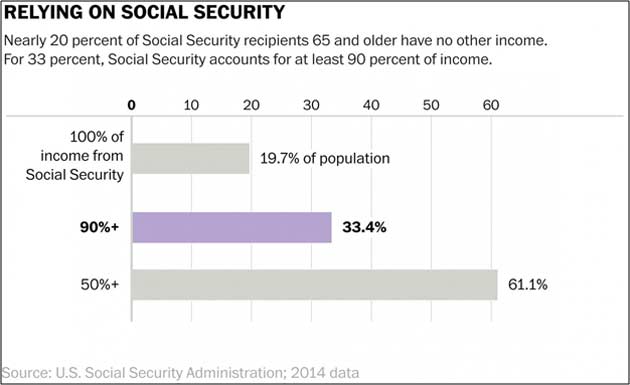

Defined Pension Plans Have Put Many Workers At Risk

Over the years, we have seen a tremendous shift in risk from companies offering pensions to workers in the private sector. According to the LBS, 401(K) and other defined pension plans have rapidly been replacing traditional pension plans. From 1980 until 2008, participants in pension plans fell from 38% to 20% of the workforce. During the same time, employees participation in defined-contribution plans rose from 8% to 31%.

This has been great for many of these workers providing they made it through the 2008 financial crisis. Since then the stock market has soared. Unfortunately, Wall Street has been ripping off many of these investors by charging them fees at every turn. Adding to the problem these workers face is that there is a good chance America is about to drop into recession.

This means stocks may be about to head downward. This could take a big toll on the retirement savings of many Americans. Of course, those in retirement and nearing retirement would feel the most pain. It does not help that Americans have been encouraged over the years to spend and incur debt rather than save. This encouragement came from politicians hooked on the idea consumer spending creates a strong economy.

This and low-interest rates for savers have resulted in many people retiring with little savings. This will leave them dependent on the government which is already deep in debt to care for them in their older years. Those of us that have studied the numbers don't see any easy way forward. Simply put, something has to give and most likely promises will be broken.

|

| While This Is An older Chart, Little Has Changed. Reality Is Not Pretty |

In our busy world that is full of distractions, many holders of 401 accounts have put them on autopilot figuring that when they need it the money will be there. All in all the factors mentioned above, including the fact that inflation is not dead, come together in a way that will leave many older Americans behind a financial eight-ball. Those in charge of such things have created a situation where with the high level of debt that exists defaults on loans could soar.

In such a situation, both businesses and investors will incur big losses. This threat to 401Ks and pension plans is real and would make many boomers collateral damage in any effort they make to correct the mess they have created. Those in or nearing retirement should make an extra effort to reduce risk and keep their savings safe.(Republishing of this article welcomed with reference to Bruce Wilds/AdvancingTime Blog)

Friday, January 5, 2024

Advancing Time: Our National Debt Has An Ugly 34 Trillion Dollar H...

Advancing Time: Our National Debt Has An Ugly 34 Trillion Dollar H...: If you have not heard, America's national debt now has a 34 trillion dollar handle. It crossed the threshold as 2024 rolled in. This is ...

Our National Debt Has An Ugly 34 Trillion Dollar Handle

If you have not heard, America's national debt now has a 34 trillion dollar handle. It crossed the threshold as 2024 rolled in. This is a sobering number and future budgets provide little hope the current trend will change. Today we are looking at an America that is running a wartime deficit at a time of peace. The emergence and acceptance of Modern Monetary Theory have turned our economic system upside down. Skeptics of its substance and sustainability have been brushed aside.

With America's national debt now blowing past 34 trillion dollars, it is important to keep the numbers in perspective. A Trillion Dollars Is Roughly $3,300 Per Person In America. Not every taxpayer, but every man, woman, and child. It is important to remember most of these people don't pay taxes.

To us who believe in old-school

economics, debt matters and is tied directly to interest rates and

inflation. For years central banks across

the world claimed a lack of inflation as the key

that allowed their QE policy to continue, however,

now that inflation has started to raise its ugly head much of their flexibility has been lost.

In short, the chart below shows, that our future is filled with huge ugly deficits.

Total Deficits, Primary Deficits, and Net Interest Outlays

|

| Data source: Congressional Budget Office. See www.cbo.gov/publication/58848#data. |

For

years the argument that "This Time Is Different"

has flourished but history shows that periods of rapid credit expansion

always end the

same way and that is in default. This also underlines the reality that

any claims Washington makes about the budget deficit being under control

is a total lie. Sadly, America is not alone in spending far more than it takes in and running a

deficit. This does not make it right or mean that it is

sustainable.

Much of the world's so-called economic growth is the result of

government spending. This has created a

false economic script and like a Ponzi scheme, it has a deep

relationship to fraud.

Global debt has surged since 2008. Throughout history, debt has always

had consequences.

Much of the massive debt

load hanging above our heads in 2008 has not gone away it has

merely been transferred to the public sector where those in charge of

such things feel it is more benign. A series of off-book and backdoor transactions has

transferred the burden of loss from the banks onto the shoulders of governments and the

people. Still, the debt exists. Shifting the liability from one sector to another does

not alleviate the problem.

When the 2018 financial year budget was first unveiled it was projected to be $440 billion. An under-reported and unnoticed report painted a far bleaker picture. The report titled the “Mid-Session Review” forecast the deficit much higher than originally predicted. The newer report predicted the deficit would come in at $890 billion which is more than double what they predicted in March of 2017.

When the 2018 financial year budget was first unveiled it was projected to be $440 billion. An under-reported and unnoticed report painted a far bleaker picture. The report titled the “Mid-Session Review” forecast the deficit much higher than originally predicted. The newer report predicted the deficit would come in at $890 billion which is more than double what they predicted in March of 2017.

We should remember that not many years ago, some Washington optimists were

forecasting that deficits would begin to decline in 2020 and that we

would

even have a small surplus of 16 billion in 2026. Since then, partly due to Covid-19 those in charge of spending have blown the

lid off that glimmer of hope and replaced it with

more trillion-dollar deficits going forward.

Back then, the summary that began on page one of the Mid-Session Review came across as a promotional piece using terms like MAGAnomicics. The report even went so far as to assure us that the deficit would fall to 1.4 percent of the GDP in 2028, from what was then 4.4 percent. It praised and touted the Trump administration for its vision and great work. This is a time when it would be wise to remember numbers don't lie but the people using them do. That report is an example of how to re-frame a colossal train wreck into something more palatable.

Back then, the summary that began on page one of the Mid-Session Review came across as a promotional piece using terms like MAGAnomicics. The report even went so far as to assure us that the deficit would fall to 1.4 percent of the GDP in 2028, from what was then 4.4 percent. It praised and touted the Trump administration for its vision and great work. This is a time when it would be wise to remember numbers don't lie but the people using them do. That report is an example of how to re-frame a colossal train wreck into something more palatable.

As

a result of the American economy having survived

with little effect what was years ago was described as a "financial

cliff" the American people have become emboldened and now enjoy a false

sense of security. Today

instead of dire warnings we hear news from Washington and the media

that this is simply another situation that we will have to navigate through, in short, it is business as usual.

The chart to the right predicted that by 2019 the national debt would

top 12 trillion dollars, instead it hit 23 trillion. Projections

made by

the government or any group predicting budgets based on events that may

or may not happen at some future date are simply predictions and not facts. This means that such numbers are totally

unreliable. The ugly truth many

people ignore is that starting in 2018 entitlements became the major force carrying the deficit higher into

nosebleed territory.

It is very disturbing that so many people have forgotten or never taken the time to learn recent financial history. By recent, I'm referring to the last fifty to one hundred years. The path that Fed Chairman Paul Volcker set right decades ago has again become unsustainable and many people will be shocked when this reality hits. Do not underestimate the value of insight gained from decades of economic perspective. It tells us the economy of today is far different from the way things have always been.

|

| In 2019, National Debt Hit 23 Not 12 Trillion dollars |

It is very disturbing that so many people have forgotten or never taken the time to learn recent financial history. By recent, I'm referring to the last fifty to one hundred years. The path that Fed Chairman Paul Volcker set right decades ago has again become unsustainable and many people will be shocked when this reality hits. Do not underestimate the value of insight gained from decades of economic perspective. It tells us the economy of today is far different from the way things have always been.

Back

in September of 2012, I wrote an article reflecting on how the

economy of today had been greatly shaped by the actions that took place

starting around 1979. Interest rates, inflation, and debt do matter and

are more significant than most people realize. Rewarding savers and

placing a value on the allocation of financial assets is important.

Many Americans living today were not even born or

too young to appreciate the historical importance and ramifications of

the events that took place back then. The impact of higher interest

rates in the 1980s had a massive positive impact on corralling the growth of both

credit and debt. Still, over the years that impact has diminished. In 1980 it was about billions of dollars of

debt, today it is about trillions of dollars. Something has gone very wrong. We should expect what is happening today to affect and shape the level of interest rates for decades.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Subscribe to:

Posts (Atom)