Thursday, December 19, 2024

Advancing Time: The Fed Should Not Follow The Path Of The BOJ

Advancing Time: The Fed Should Not Follow The Path Of The BOJ: America and the Fed may not be able to follow the path the Bank of Japan forged over the years, and it should not. Cutting rates and buying ...

The Fed Should Not Follow The Path Of The BOJ

America and the Fed may not be able to follow the path the Bank of Japan forged over the years, and it should not. Cutting rates and buying long-term bonds to artificially keep rates low may not work when it comes to the US dollar. The big difference is that the dollar is the worlds reserve currency, and the yen is not.

|

| More Fed Intervention In The Markets Destroys True Price Discovery |

A massive increase in the Fed balance sheet is a scary prospect and opens the door for central banks across the world to do likewise. This hogties the Fed's options going forward. While everything is relevant when it comes to fiat currencies, this notion is hijacked by the advantage the dollar gets from being the worlds reserve currency. Currently this advantage is fully built into valuations.

It is kind of a "weird" thought that the Fed might move in this direction voluntarily. Most likely such a shift would only occur if the global financial system was coming apart at the seams. Even then, increased intervention would not be a "cure all" and likely make things even worse.

In a past article. I built a case that the BOJ, by buying all of Japan's bonds and a huge quantity of stock market ETFs, was in effect nationalizing the country. Buying all the debt used to finance Japan's government and propping up Japan's stock market put it on the path towards owning everything. The piece focused on the flaw of creating a false and unsustainable economy. This type of action is not good for the fiat currency of any nation.

Any indication the Fed might follow the BOJ's footprint would have huge ramifications for global markets. When central banks or the government becomes a buyer they are generally don't care what the price is, this destroys true price discovery. Tied to resonable valuations are inflation expectations and long-term stability.

More intervention in markets could also unleash a bomb in the derivative markets, and that has the potential to do far more damage than any move to slash rates would create. This dovetails with the idea the Fed has painted itself into a corner. Still, we should not underestimate the many other ways and tools central banks and governments have to postpone the day of reckoning.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Saturday, December 14, 2024

Advancing Time: Revisiting, "This Time Is Different"

Advancing Time: Revisiting, "This Time Is Different": Efforts to justify the most recent market melt-up following the election of Donald Trump are difficult to comprehend if you are one of tho...

Revisiting, "This Time Is Different"

Efforts to justify the most recent market melt-up following the election of Donald Trump are difficult to comprehend if you are one of those already skeptical of this market. A read of the 2009 bestselling book titled, "This Time Is Different" did little to convince me that this time is different. It chronicles eight centuries of financial follies in which financial meltdowns have typically followed real-estate bubbles, rising indebtedness, and gaping deficits. Many of us see a strong similarity between what is happening today and prior financial meltdowns.

A read of the pdf file rather than the 2009 bestselling book titled, "This Time Is Different" delves into the history of economic bubbles. Sadly, periods of rapid credit expansion always end the same way and that is in default. The book written in 2009 by Carmen Reinhart and Kenneth Rogoff makes a solid case that despite many economists being enthralled with our newfangled Modern Monetary Theory, also known as MMT, we should still question just how well debt cycles can be managed.

The failures and meltdowns that are chronicled include state failures, bank crises, currency crashes and destabilizing outburst of inflation. Several interesting points leaped out to me while I was reading the file. One concern was the strong link found that indicated countries experiencing sudden large capital inflows are at a high risk of having a debt crisis. The preliminary evidence over a much broader sweep of history suggests this is often the case. Surges in capital inflows tend to precede external debt crises at the country, regional, and global level since 1800 if not before. Also, periods of high international capital mobility have repeatedly produced international banking crises, this is not only true during the last one hundred years but historically.

The charts contained in the working

file were frightening and a strong reminder that debt has consequences.

One thing that stands out as you read the file is that a clear pattern

and similarity exists between many of the defaults that have occurred

throughout history. The same situation is developing today as debt grows at an incredible rate globally. Much of this is the result of MMT. This economic

theory details the procedures and consequences of using

government-issued tokens as the unit of money.

|

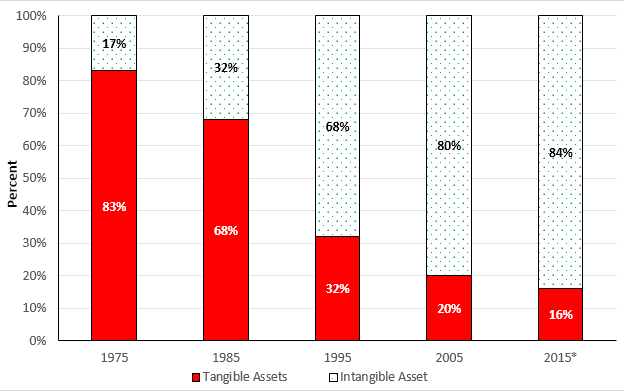

| Note Trend Of Growth In Intangibles |

According to MMT, governments with the power to

issue fiat currency are always solvent which means they can afford

to buy

anything for sale in their domestic unit of account even though they may

face inflationary and political constraints. In short MMT enthusiast

feel empowered to avoid future crashes. Of course, looking at the vast

amounts of historical data on the past financial failures that have

taken place, we naysayers voice reason for concern. MMT and what is known as the "Fed put" are part of what is fueling the growth in intangible assets.

Even the

distinction of whether the debt was held internally by its citizens or

externally by others did not alter the outcome and things still ended by

default.

The

varieties of economic crisis extend to Ponzi-type schemes

that finally collapse in upon themselves creating contagion and

resulting in a destructive domino effect. The massive derivatives market

that is touted as one of our modern financial tools is often sighted as

having the

potential to wreak havoc in this way.

Some important lessons can be garnered from the book that elevated

Reinhart and Rogoff as close to celebrity status as a couple of

economists can ever come. Over the last 800 years of financial

history we see time and time again how high government debt ratios lead

to slow economic growth. Today we are seeing deficit spending and borrowing surge as never before. It is

safe to say everyone involved in shaping economic policy should own a

copy of "This Time Is Different" and open it when things seem to be

going well because the read brings with it a blast of badly needed

seriousness and reality.

Sadly,

periods of rapid credit expansion always end the

same way and that is in default. Global debt has surged since 2008, to

levels that should frighten any sane investor because debt has always

had consequences. The massive debt load hanging above our

heads in 2008 has not receded or gone away it has merely been transferred to the

public sector where those in charge of such things

feel it is more benign. A series of off-book and backdoor transactions by those in charge has

transferred the burden of loss, however, shifting the liability from one sector to another does

not alleviate the problem.

Efforts to justify the lofty levels of today's markets, especially just a few stocks, are sometimes difficult to comprehend. Part of this is tied to the trend of passive investing coupled with the ability to leverage up and plow into speculative investments. Unfortunately, this has been deemed a good thing because it drives the wealth effect forward and bolsters the notion that pension funds will be able to keep their promises to retirees. Adding to our current market euphoria is the recent bout of financial engineering evident in companies buying back stock. All of these should be enough to give us pause, should markets falter and the wealth effect shift into reverse, the economy would be left in a world of hurt.

Despite mankind's unbridled confidence that the future will be better and our ability to blindly follow our leaders, the elevated markets of today may be placing our future at risk. Even the few people that care about such matters as the overall economy tend to be seek out easy and painless answers even if they are loosely rooted in reality. This again has raised the important issue of whether this time is really different. If not, what happens when the bubble bursts?

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Sunday, December 8, 2024

Advancing Time: Syrian Regime Collapses, Putin Loses Key Ally, Assad

Advancing Time: Syrian Regime Collapses, Putin Loses Key Ally, Assad: The Syrian government collapsed early Sunday, falling to a lightning rebel offensive that seized control of the capital of Damascus. A Syria...

Syrian Regime Collapses, Putin Loses Key Ally, Assad

The Syrian government collapsed early Sunday, falling to a lightning rebel offensive that seized control of the capital of Damascus. A Syrian opposition war monitor and two senior army officers said early Sunday that Bashar Al Assad fled the country after the collapse of his regime to HTS militants. The Syrian leader is currently unknown. It is reported he may have tried to reach a Russian airbase but might have been shot down and killed.

|

| The Fall Happened Very Slowly, Then All At Once |

Syrian rebel forces in Damascus have now declared the capital city "free" of Bashar al-Assad after nearly 25 years of rule. Former head of MI6 Sir John Sawers expressed his view to Sky News that he is surprised at how fast the Syrian regime collapsed after a lightning offensive by rebels. The offensive, led by the Islamist militant group Hayat Tahrir al-Sham (HTS) was set up in 2012 under a different name, al-Nusra Front.It pledged allegiance to al-Qaeda the following year and then, in 2016, publicly broke ranks with al-Qaeda. Still, it remains designated as a terrorist organization by the UN, US, Turkey, and other countries.

The US has even named the group's leader, Abu Mohammed al-Jawlani, as a specially designated global terrorist and has offered a $10m reward for information that leads to his capture. Jawlani, possibly to lessen opposition to his actions, told CNN on Friday that "the goal of the revolution remains the overthrow of this regime" and he planned to create a government based on institutions and a "council chosen by the people."

This rapid shift in Syria has brought about all kinds of speculation as to what happens next. This includes how many refugees might rapidly return home to Syria and how it will impact Geo-politics across the globe. This extends to Turkey, Russia, and Iran. Some of this focuses on Putin being humiliated. Putin had been a key backer of the Syrian regime for over a decade, says Bill Browder, human rights campaigner and British financier who fled Russia. This dovetails with the idea Putin and Russia are in a weakened state due to the war in Ukraine, a view that is strongly debated.

|

| Aleppo Is Just One Of The Many Cities Destroyed |

As for how optimistic we should be, we need only look at what unfolded following the regime collapse in Afghanistan, Iraq, and Libya after the fall of Muammar Qaddafi. Unstable political regimes flowing from overthrowing existing governments by force do not have as good a track record as most people tend to believe.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Saturday, November 16, 2024

Advancing Time: Economic Feast or Famine Ahead? Opinions Vary

Advancing Time: Economic Feast or Famine Ahead? Opinions Vary: Opinions wildly vary following the Presidential election as to whether we are facing an economic feast or famine. There is the notion the st...

Economic Feast or Famine Ahead? Opinions Vary

Opinions wildly vary following the Presidential election as to whether we are facing an economic feast or famine. There is the notion the stock market will continue to melt up with Trump riding to rescue America's economy. He is doing this with his new best friend Elon. This of course discounts the idea momentum is to the downside and the bull market in stocks is long in the tooth.

What some economic pendants refer to as the "everything bubble" has propelled the wealth effect forward at the same time higher interest rates have bolstered the spending of savers. It is important to remember that much of this economy has been built on this so-called "wealth effect" which has over the years come off the rails leading to economic crisis.

This leaves the question of, where things go from here. These include the effects of inflation or deflation and how they are destined to play out. Below are a few of the factors being spun by those making a bullish or bear case:

The government deficit and spending is out of control and must be cut

Tax cuts may stimulate the economy and consumer spending but may result in a larger deficit

Cutting government spending will cause many government layoffs adding to unemployment

Janet Yellen financed America's debt with short-term notes and a lot of debt needs to be rolled over

Government workers, many in unions, will be demanding huge wage increases driving inflation higher.

Increased sovereign debt will drive long-term bond yields higher.

A healthy economy flows from a vibrant middle-class based on the small businesses that we have destroyed.

Trump not known for his spending restraint, has benefited from inflation, will he now save the masses?

Will egomaniac Elon Musk with his history of feeding at the government trough put America first?

Expanding the money supply faster than the supply of goods debases fiat currencies.

Promises of higher productivity "without cutting jobs" are easier said than done.

Bringing companies and jobs home is good for America but tariffs come with some cost to consumers

Many of the things RFK is correctly advocating to make America healthy will impact company profits.

My point is that many of us who watch the economy don't agree on where things are going. The above factors and many more feed into this and the course forward may be volatile. In short, turning around many of the strong negative trends haunting America will not be easy. This will be difficult and akin to turning around a battleship in a bathtub.

A Paul Gabrial, Everything Money video titled; "My Brutally Honest Thoughts On The Great Melt Up" recently promoted his own views about a Clear Value Tax video series called “The Great Melt Up” claiming his message needed to be heard by the masses. The reason I mention this video is it does an interesting job of highlighting the problems ahead.

The effect of the concentration of wealth that has occurred has yet to be felt. We should also remember the GDP is a rather worthless gauge of economic growth considering it includes things such as non-productive government spending. It is difficult to argue the economic effect and the kind of growth flowing from the soaring debt after the Covid nightmare has been fully felt but easy to argue little good will come from it.

Of course, this only fueled a surge in the concentration in wealth and inequality that started long ago. Note the CEO-to-worker compensation ratio in America and how it has exploded over the years.:

1965 : 20.4 ---

1975 : 26.6

--- 1985 : 50.5

--- 1995 : 118.8

--- 2005 : 318.4

--- 2015 : 318.8

--- 2021 : 389 All this has been make worse by hollowing out America's middle-class by sending manufacturing jobs overseas.

President-elect Donald Trump won the 2024 election in part because working-class voters continued their migration toward the America First populism. For over a decade I have railed against Amazon a company with strong links to the government helping to destroy small businesses and communities. Still, this is a company many Americans continue to support, this proves we the masses are not as smart as we like to pretend. The task facing Donald Trump is fraught with peril.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Monday, November 4, 2024

Advancing Time: Demystifying Macroeconomic Events Is Challenging

Advancing Time: Demystifying Macroeconomic Events Is Challenging: When we take a deep dive into finance, it is like going down a rabbit hole. It is an Alice in Wonderland place where things go here and ther...

Demystifying Macroeconomic Events Is Challenging

When we take a deep dive into finance, it is like going down a rabbit hole. It is an Alice in Wonderland place where things go here and there and then twist back on themselves. This tends to all work like the edge of a cliff, or slipping into an abyss with risks increasing as we move towards the edge which in this case is a debt trap. Since everything moves along until it doesn't the risk of such an event is often discounted until it occurs.

The WTFinance videos or channel is the passion project of Anthony Fatseas. I interpret this to mean he does not pursue it to make money but because he enjoys pursuing economic and financial truth. In a recent episode of the WTFinance podcast, Anthony had the pleasure of welcoming back Alasdair Macleod. Alasdair the Head of Research for Goldmoney.

The reason this merits mentioning is because Mr. Macleod over many years has formed a lot of well-based views. Most sovereign fiat currencies are in a debt trap and politicians are showing little interest in reducing spending. One of his insights focuses on the idea that GDP increases based on government spending create the illusion things are better than they really are.

SPECULATION FUELS BUBBLES AND DEBT CREATES CRASHES

Macleod to his credit points out that debt in the public center is the problem, Growing debt in the private sector directed to increasing production is not. Macleod is Head of Research for GoldMoney and advocates for sound money through demystifying finance and economics.

For most of his career in the finance industry, he has centered much of his efforts on demystifying macroeconomic events for his investing clients.

Mr. Macleod is convinced that the government's unsound monetary policies are a destructive weapon used against the common man and we must protect ourselves from the consequences. While Macleod has a lot of solid well-based views, I contend he may overestimate the UK and underestimate America. The UK is much farther down the path to decline.

China is selling dollars because it needs to bring in wealth to fill in the holes being exposed as its economy continues to implode. As for the Chinese people's savings, when China's economy implodes much of its citizens' wealth is being sucked into a black hole never to be seen again. An example is, real estate investments gone bad. These investments yield no return and leave only the debt which often goes bad. In short, China has squandered much of the wealth that has flowed from America during the last two decades.

As always, in the comments section of the video, we find a few hidden gems. Such as: "This song was written and sung in the 1970s and here we are 50 years later." We tend to forget that eventually can be a very long time. This comment stands as a monument and reminder that some declines are long in the making. Another comment centered on, and used an interesting term I had not stumbled across before, it goes something like, Financial fuckery will be the death of us. This has occurred across the world and the financialization of everything is destroying the system.

"We Must Always Remember It's A Relitve Game"

Yes, banking

should be boring lending to real businesses that make stuff that results

in true economic growth, but it has evolved into something else. True productivity has become masked by financial gimmickry, and the economy has become a fake facade, leaving rational economic watchers to question, "where's the beef?"

Across the world, a game is being played to take the wealth generated by the working classes and transfer it to governments, this is evident in soaring national deficits and debt. This is so they can continue playing the game of appropriating it to their minions. In this case, I'm using the term "minion" in reference to, or to mean those who obey or do their bidding and follow their orders. As such, governments become the "boss" with the people becoming the servants.

Deciphering the economy is not an easy task, it is cluttered with scads of variables. This is evident in the fact economists and financial pendants never reach the same conclusion as to where we are headed. A system based on currency debasement, the wealth effect, money passively invested into retirement funds, and financial engineering through stock buybacks all add to the growth of risk. Yes, eventually, the "Fed put" based on pouring the fuel of liquidity on the fire will prove problematic.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Tuesday, October 22, 2024

Advancing Time: Tariffs Are A Way Of Putting A Finger On The Scale

Advancing Time: Tariffs Are A Way Of Putting A Finger On The Scale: Tariffs are a way of putting a finger on the scale, metaphorically speaking. While we are hearing the negatives about how they raise prices ...

Tariffs Are A Way Of Putting A Finger On The Scale

Tariffs are a way of putting a finger on the scale, metaphorically speaking. While we are hearing the negatives about how they raise prices for consumers, they also have the positive effect of making products made in our country more competitive in our local market.

:max_bytes(150000):strip_icc()/Tariff-4188187-final-070716a9bd23499d861283857dad0cf0.png)

It is wise to remember that companies in many other countries are not burdened by paying workers healthcare costs or in many cases, any type of benefits. This gives them a tremendous advantage even before factoring in wages that are often a fraction of those paid in more developed societies. Also, if you add in subsides they are getting from their government it is game over

This all flows back to the importance of where and what consumers buy matters a great deal when it comes to a nation's economic health. Considering that free trade is not necessarily fair trade, makes using a finger to balance the scale even more necessary. This becomes very clear when looking at China's plan to export millions of low-cost EVs into countries. With our domestic manufacturers unable to compete, without tariffs, they would go out of business.

How can a company in America that is forced to pay high wages, provide expensive medical coverage, and pay for benefits such as paid holidays and vacations even think about competing with those that don't? To make matters worse, countries such as China, that under stand the value of providing workers with jobs, tip the scale even further. They do this by giving companies subsidies in many forms, some less visible than others.

While people involved in giving investment advice such as Rick Rule take the stand tariffs are simply a tax around 18 and a half minutes into this video, that view is a bit simplified. What Rule fails to take into account is that fair and free trade are not the same thing. Cheap goods entering a country may help lower costs to consumers but they have a hidden cost.

The claim that tariffs are a tax has some merit. Still, if you agree that there is no such thing as a free lunch, then you should be open to the idea that entitlements need to be paid for in some way or form.

In short, we need productive jobs, this means jobs that build things and create wealth, not simply keeping people occupied. Without people in America working and paying taxes, outsourcing the production of the goods we use to other countries is not sustainable. Trade deficits bleed a country of its wealth and result in debt.

When a county, like China, subsidies production which lowers cost, they crush the fairness we expect when it comes to trade. Plugging the holes in a trade system that is not as transparent as we tend to think is not easy. An example of this is how China exploits the rules by using Mexico as a way to get goods into America by sidestepping tariffs.

Tariffs are a way to protect domestic producers and halt jobs from being pilfered by exploiting nations like China. History has many examples of empires being created by those who understand the power of selling far more than you buy. Fortunately for America, China has squandered its opportunity to accumulating great wealth through stupidity and corruption. The evidence of China's missteps are visible in its ghost cities and first-class infrastructure in the middle of nowhere.

Some economic watchers have warned that increasing the number and amount of tariffs could escalate into a global trade war with massive ramifications. This occurred during the Great Depression, I think the danger of this is overblown. Most rational people understand the best result of trade is to create a win-win situation. Trade imbalances generally fail to accomplish this.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Wednesday, October 16, 2024

Advancing Time: Fox Grilled Vice President Kamala Harris On Issues

Advancing Time: Fox Grilled Vice President Kamala Harris On Issues: Vice President Kamala Harris was grilled by Fox News chief political anchor Bret Baier on 'Special Report. In just over a 25-minutes, ...

Fox Grilled Vice President Kamala Harris On Issues

Vice President Kamala Harris was grilled by Fox News chief political anchor Bret Baier on 'Special Report. In just over a 25-minutes, they discussed immigration, the economy, responding to U.S. adversaries, and more. Prior to the event, there was a great deal of fanfare about Harris's courage to enter the lion's den and face what was predicted to be a tough interview that might well decide the Presidential election.

Immediately after the interview, the left-tilting media rushed to paint a picture of a triumphant Harris not only surviving the ordeal but dispelling all doubt as to her ability to field tough questions. Also, it seems, that claims Baier was overbearing and rudely interrupted Harris were also put out there to create sympathy for Harris.

Surprisingly, this important interview was a bit difficult to find on the internet, but when located and watched in its entirety, viewers may come away with a different opinion than what many newsgroups alleged. Many of the almost 20,000 comments below the interview video focused on her not answering the questions, blaming everything on Trump, and telling Baier, "come on, be honest, you know what I mean." Below are a few of those comments:

*She spent 27 minutes blaming a man who hasn't been in office almost 4 for yrs for everything.

*Always Trump's fault yet she's been VP for 4 years. Deflect, deflect. I LOVED how he pushed her but she still didn't answer his questions.

*I am not a Trump supporter. With that being said, it is beyond infuriating watching her refuse to take responsibility for ANYTHING.

*The woman who never earned a single vote in a primary is concerned about "democracy." You just can't make this up.

*When your main platform is to criticize the opposition, it simply means you have no platform.

There is no reason to bore you with more, here is the link to the interview, decide for yourself. https://www.youtube.com/watch?v=80DaR2CVNNk

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Sunday, October 13, 2024

Advancing Time: MISINFORMATION, Using Doublespeak As Censorship

Advancing Time: MISINFORMATION, Using Doublespeak As Censorship: The word of the day is misinformation. Those using it are often trying to censor speech and opinions, which they call "dangerous,&quo...

MISINFORMATION, Using Doublespeak As Censorship

The word of the day is misinformation. Those using it are often trying to censor speech and opinions, which they call "dangerous," in an effort to silence those they oppose. Labeling the views of those you oppose as misinformation that must be squelched is a way of utilizing "doublespeak" as a form of censorship.

The claim someone is spreading misinformation diminishes the message of your opposition or detractors. It implies they are lying or simply do not know what they are talking about. When put in context, it also reinforces the idea "me good, them bad" even though it requires no proof the accuser is telling the truth.

Doublespeak is defined as language that deliberately obscures, disguises, distorts, or reverses the meaning of words. This can be in the form of euphemisms, such as "downsizing" for

layoffs and "servicing the target" for bombing a location. Doublespeak is

primarily used to make the truth sound more palatable. The flaw in what you have read is this is not just about doublespeak but something far more sinister, it is about something bordering on straight-out lies.

The term "doublespeak" flows from concepts in George Orwell's novel, Nineteen Eighty-Four. This term, as well as "Newspeak" are not used in the novel but are descriptions of the misleading type of speech often used to deceive. Screaming that something is misinformation and those spreading it are awful immediately paints them as unreliable or dishonest. At the same time, it is a way of elevating the speaker or writer to a higher plane of honesty.

Declaring a message as misinformation and not directly answering a question are powerful weapons in burying the truth and spreading propaganda. It opens the way for someone to take us down the path where they can spout scripted platitudes and prepared sound bites. Sadly, this has become our world, and it seems, polarization will continue to only make it worse. This is a reason to be wary of those slick talkers gifted in promoting their agenda.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Friday, October 11, 2024

Advancing Time: The Fed And Its Muddy Path Forward

Advancing Time: The Fed And Its Muddy Path Forward: The Fed's biggest failure is seen in not forcing the government to cut spending and allowing it to pile up massive debt. The Fed's ...

The Fed And Its Muddy Path Forward

Not forcing the government to cut spending and allowing it to pile up massive debt can be seen as the Fed's biggest failure. The existing massive sovereign debt makes the Fed's path forward a matter of great debate. When describing its options, terms such as "painted itself in a corner" are used. This indicates many people understand the Fed is not limited in its options but will face great difficulty in arriving at a good outcome.

Insanity and madness in the financial system and politics have reached the point where it has become normal. This is evident in many areas of our society. Little noticed was Jill Biden recently running a cabinet meeting like

this was a normal part of the First Lady's role in Washington. This comes at the same time assassination

attempts on Trump, a Presidential candidate and former President, are seen as no big deal. These dovetail with claims we need an interest rate cut when markets are making new highs.

With equities, gold, and many other markets hitting all-time highs,

the Fed cut rates 50 basis points. How do we reconcile the idea we must

rapidly cut rates if the economy is doing so well?

Circling back to economics, around six minutes into a recent video, Daniel Lacalle, author and professor of economics, mentions the unmentionable, unfunded liabilities. He also makes it clear that America is not alone or positioned as poorly as many other countries. Laccalle then moves into an in-depth discussion on shifts now occurring. Lacalle also covers much of the unfunded liabilities in a much shorter six-minute video that points to the debasement of currencies and more loss of purchasing power in the future. The link to that piece is; https://www.youtube.com/watch?v=PmUAxI_M9oE

Very troubling is his case that we have seen nothing yet. Lacalle claims we are on a course of “monetary destruction” that will get far worse as we move towards the 2030s. This has created a situation where some investors are already moving towards strategies that safeguard their wealth in uncertain times. This includes things such as negative interest rates, bank bail-ins, and the topic of de-dollarisation. Financial repression is not implemented to give us choices but is a tool to shift wealth away from the people and to the government.

As already noted, the Fed is not alone, central banks across the world have miserably failed to contain government expansion and spending. In the minds of many investors, it is odd that the price of Gold going higher at the same time many economic pundits talk about falling into a deflationary recession or worse. If gold and dollars rise together this is of course in relation to all other fiat currencies. Still, there is the problem that as the dollar rises in relationship to other currencies it creates havoc in global markets.

The fact is, much of the power of central banks flows from being able to inject liquidity into the market during times of turmoil. Their Achilles heal or weakness, which many people have yet to understand, is their limited ability to control the long end of the rate curve. This refers to long-term interest rates, these rates are more dependent on investors' sentiment and views of currency debasement and inflation.

The recent volatility blamed on an unwinding of the Japanese carry trade highlights how the relationship in the value of fiat currencies can pack a wallop. Even as this is being written, we have economists and economic advisers pointing in all directions when it comes to where markets are going. Some are predicting a melt-up, some are declaring "clear skies ahead," and others that the economic wheels are about to fall off the bus.

When it comes to those controlling the Central Banks making decisions that determine the course we take, it would be wise to remember they do not have total control of the situation. We may find they chose the wrong course, their tricks, or even changing the rules are ineffective. In a past posting, I pointed out that given enough pressure they might, even if it is a bad decision, again open the gates and flood the system with a plentiful supply of cheap money.

We should marvel at how far Fedspeak, wordy, vague, and ambiguous statements, has gotten us so far. This is amazing considering how broken and dysfunctional the financial system has become. The crux of this post is that we live in unusual times and we should expect conditions around us to be both unpredictable and volatile. Factor in the coming election, the drumbeat of war, and what is happening in the area hit by Hurricane Helene, and it is clear, that we live in interesting times. With this in mind, it is difficult to envision the Fed will be able to continue successfully threading the needle.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Sunday, October 6, 2024

Advancing Time: Helene, Government's "Total Fail" During A Major D...

Advancing Time: Helene, Government's "Total Fail" During A Major D...: Yes, it's happening. Following Hurricane Helene, we are witnessing a total failure in the government's response to a major disaster....

Helene, Government's "Total Fail" During A Major Disaster

Yes, it's happening. Following Hurricane Helene, we are witnessing a total failure in the government's response to a major disaster. Reports on NBC, as well as hundreds of others give us some insight as to some of the problems people across western North Carolina are facing. With roads, bridges, water pipes, and electrical lines washed away, FEMA is telling us they don't have the money to "Git er done." It seems the money has gone to aiding immigrants at the border and providing weapons for Ukraine.

|

| During Disaster, Real Help Is Hard To Find |

Desperate families are still waiting for word about missing loved ones, days after the flooding disaster in Tennessee, and North Carolina. Expect politicians to fill the slots in the mainstream media to spin the reality on the ground into a tale of "we are getting the job done" The fact is, they are not.

Fast-talkers, such as Pete Buttigieg, will vigorously paint a picture that the Biden /Harris team in Washington has risen to the task. Sadly, the history of people like Buttigieg, the equivalent of a modern-day snake oil salesman is to twist the truth. As one of Kamala Harris's prime damage control go-to guys, it is his superpower to capably paint a glorious picture, over-promise, and then underperform.

Buttigieg will concede that while this is terrible, efforts are continuing to be ramped up and things are under control. He is unlikely to adequately address the issue of why many of those with feet on the ground are being told by government authorities to stand down under penalty of arrest. This includes efforts to seize aid materials flowing into the area under the idea they need to be "inventoried" and redirected to the proper agencies.

In the middle of 2022, an article on AdvancingTime cautioned on how during a major disaster nobody should count on help from the government. It has been a long time since America has had a really good leader. Sadly, the damage these "less than stellar" Presidents cause a lot of problems for society that can linger for decades. With this in mind, it should be noted that bad leaders have a habit of opening Pandora's box for the greater good whenever a disaster strikes. It seems, to some politicians, that the only way the government can help us during a crisis is to focus on taking more control over our lives.

At that time, some Freedom of Information Act (FOIA) documents released by the George W. Bush Presidential Library spotlighted the powers that modern presidents "claim they possess" in moments of crisis. Following 9-11, this type of expanding the President's powers could be viewed as a pure power grab. In short, during a national crisis, governments seem more interested in control than coming to the aid of their citizens.

The "presidential emergency action documents" (PEADs), were created during the cold war. Back then, many people feared we might be attacked with nuclear weapons. These documents authorized the president to enact measures such as suspending habeas corpus, detaining "dangerous persons" within the country, censoring news media, and even preventing international travel.

The desire to extend power dovetails with today's high-profile disasters where the media generates the feeling our government stands ready to rush to our aid in case of a national disaster. Following a tornado or hurricane in the news, we often see FEMA workers spread out and moving from door to door offering help to Americans in need. This reassuring media coverage is misleading. The truth is if you find yourself in a large area of devastation due to a crisis or disaster the government will prove largely ineffective.

What is occurring in the areas devastated by Hurricane Helene is proof that when a large Armageddon event does occur people affected quickly find that God helps those who help themselves.

The trend of pandering to victims that we have seen develop over the

years may be a result of the battering former President Bush took in

opinion polls following Hurricane Katrina. The pictures that the media

posted following a slow response in handling Katrina haunt his

administration and paint Bush as being insensitive and out of touch with

the plight of poor Americans. Unfortunately, claiming the government is

responsible for dispensing sorrow and grief does not result in repairing communities and lives torn apart in a disaster.

Over the years in our media-driven world, the President has adopted

the

role of "consoler in chief." This means they are expected to pour forth

sympathy and

cast out concern for every American following incidents of destruction

or violence. It does not matter if it is an accident, shooting, or some

natural disaster, in recent years all this has reached new heights where

even in the case of a few deaths it is not uncommon to see the

President leaping upon Air Force One and rushing to the scene or calling

to express a huge dose of heartfelt sympathy. In this politically

correct world,

it has even gone so far as to the President being expected to weigh in

on minor tragedies that occur throughout the world.

It should be noted that much time is wasted performing these acts that

could be better used and focused on solving many of the real and

pressing problems that face America. In reality, this pandering is a

major disservice to Americans, it fosters the impression the

government will be there for you if you ever get into a pickle or jam. While

reassuring to many the false illusion of a competent and effective

government ready to come to your aid comes at the cost of raising

unrealistic expectations.

I suspect that with the formation of the massive Homeland Security Agency, this may be a case of reassuring the masses that their tax money has not been wasted, while it is. A perfect example would be the government's reaction to the Boston Marathon bombing. The response was overwhelming, but in the end, it was a homeowner checking the tarp on his boat who noticed a spot of blood and not the thousands of law enforcement officers that brought the manhunt to an end.

|

| No Government Is Ready For This! |

It is important to remember, that all disasters are not created equal. There is a huge difference between a tornado and a nuclear bomb going off in a major city. Also, what happens if the power grid fails and electricity is lost over a large area for a long time during inclement weather? In all reality, the Federal government would be relatively ineffective and not much help in a major crisis that covered a large area and affected tens of millions of Americans.

Anyone who has ever experienced the frustrations caused by a bad storm with power outages and such will tell you most help comes from nearby and government is not the answer. People who adopt the attitude that they are victims following a major disaster and wait for government help to arrive should expect to wait a very long time. Anyone counting on the government is making a huge mistake, simply waiting for help can be the kiss of death. Still, the government should be doing a hell of a lot more to aid people in this disaster than they are. This indicates a total failure on the part of Washington.

Footnote: Regardless of what you have been told, it is the people of this great nation that made America famous, not the government. Here is the link to a very moving 1974 Harry Chapin song that vividly captures this notion it is titled: "What Made America Famous."

(Republishing of this article welcomed with reference to Bruce Wilds/AdvancingTime Blog)

Sunday, September 29, 2024

Advancing Time: Pete Buttigieg Is A Modern Day Snake Oil Salesman

Advancing Time: Pete Buttigieg Is A Modern Day Snake Oil Salesman: Some politicians seem destined to be around for a long time. Washington is a place where even the worst kind of creatures can not on...

Pete Buttigieg Is A Modern Day Snake Oil Salesman

Some politicians seem destined to be around for a long time. Washington is a place where even the worst kind of creatures can not only survive but thrive long after what should be their "expiration or past due" date. While still somewhat new to the scene, Pete Buttigieg is the equivalent of the modern-day snake oil salesman. The history of these guys is to twist the truth, paint a glorious picture, over-promise, and then underperform.

Pete Buttigieg, the former two-term mayor of South Bend, Indiana, can often be found at the intersection of ambition and disingenuous. Currently. the Democrats are busy putting lipstick on the pig known as Kamala Harris and Buttigieg is being brought forward to convince us she is not a pig.

Because he is so damn good at artfully spinning reality does not mean he has any other redeeming qualities. His flare for this does however make him the go-to man for preparing Vice presidential nominee Tim Walz to debate Ohio Sen. JD Vance. According to a Harris campaign official Buttigieg is standing in for Vance during Walz's preparations.

On February 2, 2021, Buttigieg was confirmed as President Biden's secretary of transportation, this made him the first openly gay man to serve as a cabinet secretary. It could be argued that he was given this high position in the Biden administration in return for folding his 2020 Presidential bid and throwing his support behind Joe Biden. The fact evident when evaluating his job performance.

|

| Buttigieg Was Given An Important Job That He Is Not Qualified For |

Two terms as mayor of a city with a population of only 103,000 residents and seven years as an officer in the U.S. Navy Reserve does not give a person the background to be the secretary of transportation. This massive job is to oversee many aspects of transportation policy by federal agencies within the US Department of Transportation. The decisions flowing from this department are destined to have long-term and profound impacts on the economies and lives of Americans for decades. This includes, are you ready? Overseeing 58,622 employees and deciding where and how much nearly a TRILLION dollars of government money will be spent.

- Highway administration: Via the Federal Highway Administration (FHWA), the USDOT builds and maintains national highways, funds state highways, and sets safety standards for infrastructure projects.

- Passenger vehicle safety and standards: Via the National Highway Traffic Safety Administration (NHTSA), the department sets safety standards, emissions standards, and public safety codes.

- Commercial vehicle safety and standards: The department's Federal Motor Carrier Safety Administration (FMCSA) functions much like the NHTSA, only for commercial vehicles.

- Aviation safety and standards: Within the USDOT, the Federal Aviation Administration (FAA) sets rules, regulations, and safety standards related to the nation's air travel.

- Railroad Administration:

The DOT operates the Federal Railroad Administration (FRA) to regulate

standards and safety among the nation's railways.

- Maritime Administration: The Department of Transportation governs maritime transportation through two agencies, the Maritime Administration office (MARAD) and the Saint Lawrence Seaway Development Corporation (SLSDC), which concerns itself with the Great Lakes.

- Protecting public health: Through the Pipeline and Hazardous Materials Safety Administration (PHMSA), the department seeks to prevent the release of harmful pollutants through pipelines.

- Granting funds to states: In addition to financing and building federal transportation projects, the USDOT funds state transportation initiatives via the Federal Transit Administration (FTA).

In short, his fast rise in the political arena has placed him in a position he is

inadequate to perform garnering him a fair amount of criticism. His being ambitious is not the problem, his combining it with dishonesty

while artfully promoting a dubious agenda and poor policies is the problem.

Under the title of "Beware of slick talkers." while it escaped the notice of many Americans, our new Transportation

Secretary was caught a while back on video pulling one of those stunts that

prove politicians untrustworthy. Buttigieg arrived at a meeting on a

bicycle to give the impression he rode there when in fact he had been

carried most of the way in a gas-guzzling SUV.

| Buttigieg's Book Title; "TRUST: America's Best Chance." Underlines His Hypocrisy |

Ironically the book authored by Buttigieg and published in 2006 is titled; "TRUST: America's Best Chance." This underlines the hypocrisy and importance of knowing that America's new Transportation Secretary is a lying turd, or if you prefer a less harsh way of saying this, a modern snake oil salesman. Part of Buttigieg's "stick" is to have people refer to him as Mayor Pete or Secretary Pete to make himself appear more accessible and more like them.

For a clear picture of just how well this political creature has carved his way into power, watch this piece where Pete Buttigieg talks to Jon Stewart

about why he goes on Fox News; https://www.youtube.com/watch?v=jli0_oKMG-0 It is clear Stewart's audience is giddy for Pete and the comments under the video confirm this "love fest," things such as ;

When Pete Buttigieg was running for POTUS in 2020, I worked on several of his rallies in Charleston SC. I saw him on the stump and "backstage." He is very articulate, well-read, smart as a whip, and firmly in control of his emotions. I would vote for Pete Buttigieg for ANYTHING in a skinny second!

Every time hear Pete Buttigieg speak I feel more hopeful for the USA.

As a British person, I'd never heard him speak before. Comes across as super articulate, measured, dignified, and capable. Imagine the future with someone like him in higher office.

I watch everything Pete is on. Can't wait until he becomes POTUS.

All this puts Buttigieg in the role of damage control and major Harris cheerleader. Also, it is likely we will be seeing a lot more of Pete in the coming months and years. In a video put out on July 28th Buttigieg goes down the path of calling and describing JD Vance strange and weird. If you haven't gotten the memo, declaring conservatives and their ideology as weird is the democratic code weird. Politics should be joyful Democrats declare in this video as they deliver their message with a thick blanket of fear-mongering and how Trump will rob Americans of their freedom. I end this post with the simple warning, "Beware of slick talkers." When combined with modern media they are always a clear and present danger.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Tuesday, September 17, 2024

Advancing Time: Fed's Interest Rate Cuts May Not Bring Strong Economy

Advancing Time: Fed's Interest Rate Cuts May Not Bring Strong Economy: As the Fed begins to cut interest rates, it is important to consider the possibility that lower rates will not produce a stronger economy. W...

Fed's Interest Rate Cuts May Not Bring Strong Economy

As the Fed begins to cut interest rates, it is important to consider the possibility that lower rates will not produce a stronger economy. We only need to look at Japan to see the proof an economy is about far more than just interest rates. Feeding into this is the Fed's limited ability to directly determine rates at the long end of the curve.

Lower rates have almost been guaranteed and promised, however, we should never forget that liquidity is far more important. This is why a past article here on AdvancingTime touted the idea more focus should be placed on liquidity rather than interest rates. When you need money, whether the amount is small or large, not being able to get it can lead to a life-changing or grave outcome. Yes, it is possible rates can fall at the same time credit tightens. This can result in dire consequences.

Contagion is a word used to describe how a disease is passed from one individual to another. It is also used to explain how problems in one area of the economy tend to spill over into other sectors of the economy and markets. When it does it can occur quickly and be devastating to the financial system. This is why it would be wise to remember that if you have good credit you will always be able to get a loan a myth.

People learn in a credit crunch that liquidity is far more important than interest rates. Many years of an easy credit environment have numbed people to the reality that credit is not a guaranteed right. This is a reality that can hit us like a slap in the face.

Part of what we will see in the coming months could be simply an adjustment

in the flow of capital to those who want it most or can afford it. Much of what may develop is a lack of willingness to lend based on the possibility the risk

of not being repaid increases in a difficult economy. This has the potential to create a self-feeding loop in

a credit-tightening cycle. Halting such a damaging loop can come down to the Fed's questionable ability to get banks to lend during adverse conditions.

The notion you stand a snowball's chance in hell of getting a loan in an environment of credit tightening has yet to dawn on many people. The existence of so-called "loan sharks" underlines the idea that if someone is desperate to borrow money they will often put themselves in danger to do so. Loan sharks, which generally operate outside the law, offer loans at extremely high interest rates and have strict terms of collection if the loan is not repaid.

Most people have not experienced cycles of severe credit tightening and may have difficulty imagining such a scenario. This is partially due to what may be considered "memory bias" or "recency bias." This can result in confusion as new situations arise. Memories tend to be clouded by people incorrectly believing that recent events will likely occur again. This tendency obscures the probability the future may be quite different from the past and leads people to make poor decisions based on the recent past.

Like many businesses, the banking sector has changed over the years. The banking industry is far different than it was a few decades ago. As a financial institution, banks are licensed to accept deposits and make loans. Not only do banks protect our money, they lend out this money to create profits. But they also perform a lot of other financial services. That said, banks are not shy about placing upon customers a lot of fees and other charges.

- The three main business segments for a bank are retail banking, wholesale banking, and wealth management.

- Retail banking or personal banking involves deposits, mortgages, loans, and credit cards.

- Wholesale banking is related to sales and trading and mergers and acquisitions.

- Wealth management generates revenue through retail brokerage services and asset management.

The simple and ugly truth is banks are not "good neighbors" there to serve and be concerned about the community.

Banks do not make much money on small loans at low-interest rates. The

cost of making these loans far outweighs the income flowing from them

even before factoring in the risk of default. This is why most small

businesses must turn to other sources in order to find financing and a

lot of these are loans "hidden off the balance sheet" at much higher

rates. When push comes to shove, the banks will be fast to throw you under the bus. Adding insult to injury, if you have put assets up with them as collateral, they may be inclined to seize them if doing so plays to their advantage.

| Interest Rates Have Fallen Over The Decades |

Liquidity is the lifeblood of commerce.

The massive growth in the financial sector versus Main Street, the GDP,

and the real economy has made debt a major concern. Credit markets will

be coming under a lot of pressure as a great deal

of this debt coming due. Adding to the problem is that much of it is

short-term debt that must be rolled over or extended. It will be

interesting how this plays out in a "risk off" environment. It is just one of the factors helping to determine where investors park their wealth and in what form.

Lately, the

Fed has been boxed in by the hyper-reaction of investors to anything it does.

It needs to get investors to refocus on profits, margins, and risk. The

combination of cheap money, and too much of it, has fueled speculation

and blown the lid off markets in recent years. It seems that greed has overshadowed the degree a

tightening in credit standards can impact the economy. This is partially

due to either the Fed's or the government's willingness to generate stimulus that promotes the wealth effect.

The growth generated from low-interest rates and easy credit has some drawbacks.

This takes us to the issue of where the stimulus is coming from. Consider that stimulating the economy through monetary policy and stimulus from fiscal spending have different long-term implications for

inflation. It also impacts the economy in a big way, especially when it is not geared towards increasing productivity.

This has fostered an environment where the stock market has been less efficient in discovering the true

value of companies. While

recessions halt inflation the issue is just how much irreparable damage

it will inflict on Main Street and society as the "lag effect" hits us

in the face. The stock market is not cheap, earnings will most likely

fall takeing stock prices with them. In response, expect tapped-out

consumers to cut back on spending, unemployment to rise, and a lot of

small businesses to fail.

A lack of liquidity can be poisonous. When you need money, whether the amount is small or large, not being able to get it can lead to a life-changing or grave outcome. It is important to point out that housing values are a far bigger issue for most Americans than stocks. Still, these markets do influence each other. Dealing with a "bubble economy" is always a problem and results in investors and people, in general, to buy high and sell low, often with devastating consequences.

(Republishing of this article welcomed with reference to Bruce Wilds/AdvancingTime Blog)

Subscribe to:

Posts (Atom)