Thursday, February 29, 2024

Advancing Time: The Dreadful "C" Word - Conserve!

Advancing Time: The Dreadful "C" Word - Conserve!: An article I wrote years ago remains as relevant today as when I wrote it. The subject delved into how candidates shy away from the dreade...

Sunday, February 25, 2024

Advancing Time: Austerity Appears To Be An Idea Long Dead

Advancing Time: Austerity Appears To Be An Idea Long Dead: A word nobody has mentioned for a long time is austerity. The term that would take us down the path to sustainable spending has been tossed ...

Austerity Appears To Be An Idea Long Dead

A word nobody has mentioned for a long time is austerity. The term that would take us down the path to sustainable spending has been tossed into the dustbin of history. Today the concept of government restraining spending is considered a bad idea. Those who oppose austerity often cling to the idea that a major reduction in government spending will change future expectations about taxes and future government spending. These are factors that encourage private consumption and propel forward overall economic expansion.

Since 2017 when an article by James McCormack titled, "The Quiet Demise of Austerity" was published on Project Syndicate, the idea of austerity has become toxic. Government spending has gone over the moon. It is a reach to blame it all on governments' response to the Covid pandemic. Still, the fact is that since then America's national debt has soared from roughly 21 trillion to over 34 trillion dollars. In short, austerity seems to have been forgotten just when it is needed most.

In his article, McCormack pointed out that debates about the potential advantages of using stimulus to boost short-term economic growth, or about the threat of government debt reaching such a level as to inhibit medium-term growth, have gone silent. It is as if the whole world has capitulated to the idea that we can spend our way out of the debt. Other arguments center on the idea that it really doesn't matter and that we will deal with the issue when we have to.

There is no doubt that economic growth tends to mask a multitude of problems. In economics, austerity refers to cutting spending often by lowering and reducing the number of benefits and public services. Austerity policies are often used by governments to try to reduce their deficit spending. Spending cutbacks are sometimes coupled with increases in taxes in an effort to demonstrate long-term fiscal solvency to creditors.

|

| Austerity Is Often Seen As Heaping Misery On The Poor |

In

the article I cited McCormack wrote; Objections to austerity

were understandable after the 2008 financial crisis when growth was

languishing below 2% and sizeable negative output gaps suggested that

overall employment would be slow to recover. But now the merits of

austerity seem to have been forgotten just when it is needed once again.

It is true that government spending financed by deficits does support economic growth when consumers and businesses are unable to do so. When the private sector is unable or unwilling to consume at a level that increases GDP and employment sufficiently, Keynesian economists claim governments should spend more, and not less. This tends to be a slippery slope that is difficult to exit. Adding to this problem is that the government sector tends to be the least productive part of the economy. Larger government often leads to more regulation which strangles productivity in the private sector. What we are witnessing today is spending more and more in order to achieve economic growth.

Austerity has been given a bum rap, blaming it for the problems we face is akin to blaming the medicine taken after someone becomes sick for the illness. Austerity measures have been associated with public protest and claims of a significant decline in the standard of living. The argument by contemporary Keynesian economists that budget deficits are appropriate when an economy is in recession bolsters this movement. They claim it reduces unemployment and helps spur GDP growth, and that in an economy one person's spending is another person's income. If everyone tries to reduce their spending, the economy can fall into what economists call the paradox of thrift which results in a reduced spending spiral and a fall in the GDP.

Austerity measures are typically taken in extreme situations where there is a threat that a government cannot honor its debt liabilities. Such a situation may arise if a government has borrowed in foreign currencies that they have no right to issue or if they have been legally forbidden from issuing their own currency. In these cases, banks and investors may lose trust in a government's ability and/or willingness to pay its obligations and either refuse to roll over existing debts or demand extremely high interest rates.

Often the typical goal of austerity is to reduce the annual budget deficit without sacrificing growth. Part of the goal of these policies is generally to reduce the overall debt burden, as the economy grows. Unfortunately, most efforts by central governments to prop up asset prices, bail out insolvent banks, or "stimulate" the economy and deficit spending make stable growth less likely.

People often look for someone or something to blame for the troubles we bring upon ourselves. This is especially true when austerity is introduced as a way to bring out-of-control government spending back in check. Austerity has negative connotations because it is often painful. Still, blaming austerity for the blowback from governments living beyond its means is more than unfair.

Common logic would dictate at all times governments operate with responsible reigns on spending. If a government spends and runs its business in an austere way the issue of when to start cutting or tightening should never surface. There is no doubt that economic growth tends to mask a multitude of problems. In economics, austerity refers to cutting spending, often by lowering and reducing the number of benefits and public services.

Simply put, such cuts are very unpopular and painful to the people and the voters as social spending programs get targeted for cuts and taxes are raised. Also, retirement ages may be raised and government pensions reduced. Even port and airport fees, train and bus fares, and a slew of other cost usually increase. Please note that while it is important to control rising budgets and how much is spent, where it is spent is just as important.

The problem we face today is the wild spending post-Covid never stopped. Every dollar wasted on political pork, fraud, and poorly considered infrastructure makes the country's fiscal situation even worse. Those opposing austerity argue that, in periods of recession and high unemployment, austerity policies are counter-productive, because reduced government spending can increase unemployment. Also, reduced government spending reduces GDP, which means the debt-to-GDP ratio examined by creditors and rating agencies does not improve.

At some point, the present and the future intersect, it is not just about the deficits of today but the promises you make coming due. These promises and how they affect the financial landscape must be factored in. The bill for overspending does eventually come back to haunt you. That is why we would be far better off if the concept of austerity was replaced or renamed sustainable spending. I suspect that by the time cutting spending is again in vogue, we will be in real trouble.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

Friday, February 9, 2024

Advancing Time: What Data Should Investors Believe? It Is All Skewed

Advancing Time: What Data Should Investors Believe? It Is All Skewed: Where are these "consumers are confident" stories coming from? Recent Michigan consumer confidence numbers are up. This comes at a...

What Data Should Investors Believe? It Is All Skewed

It seems that many consumers are convinced the Fed will soon drastically drop interest rates and it will be a big boost to the economy. To many younger people, decades of lower interest rates are the only thing they have ever known. The problem here is that lower rates do not necessarily lead to a stronger economy.

Part of the problem is that we are seeing the best of this data being revised downward month after month. This news is generally not highlighted on the front page but buried where it is less noticed. What could go wrong in a system where the President has been declared so mentally impaired that he cannot be held responsible for handling documents related to our security and safety?

While Americans seem unable to stop spending, signs are rising that we are reaching the point where lenders would be foolish to extend more credit to them. Today credit card debt is at an all-time high, car repos soaring, commercial real estate is close to crisis mode, and consumer savings rates are very low. All these trends point to trouble ahead.

Adding to these woes is that inflation is

not done, residential housing affordability is terrible while the fed

deficit soars and unfunded debt obligations are creeping up. In some sense, it is pathetic that some investors' bright hopes are centered on history's record of Presidential collection years as being positive for the stock market. This is clouded, of course, by something we have heard a lot about, and been warned about, recency bias.

This is our tendency to overemphasize the importance of recent experiences or the latest information that we have witnessed when estimating future events. Recency bias often takes us in the direction of thinking that recent events are more of an indication of how the future will unfold than they really are. Considering the direction of the stock market for decades, recency bias paves the way to thinking other than a few short-lived pullbacks it is always up, up, and away.

Still, some of the data coming out is concerning. If you take a close look at job creation numbers you will find that as of late an explosion in the number of new jobs being created in the government and its money-funded healthcare sector. This is not good news, a healthy economy needs private sector growth. There is evidence we may soon start to see private sector layoffs soar as companies try to remain profitable when they are forced to refinance debt at higher interest rates.

The Bureau Of Labor Statistics (BLS) birth-death model may be skewing much of the current employment data. Part of this is due to the increased use of Employee Identification Applications also known as EINs. The need to have an EIN is tied to getting a 1099 tax form which in 2000 was dropped from 20,000 dollars to 600 dollars.

This has promoted many new applications for the easy to apply for EIN. However, these are not new businesses or increasing employment simply moving existing commerce into another part of the economy. Here it is important to remember, that many new businesses don't amount to diddly-squat. Most close within a year often leaving behind unpaid bills. Unpaid debts may create jobs but not the productive kind the economy needs.

When trying to get a handle on where the economy is headed, it is also important to consider data showing the personal savings rate has collapsed. Data reports indicate for many people, real income is down. This means many people are living paycheck to paycheck. In short, people do not have discretionary income to save even with a record number of people working more than one job.

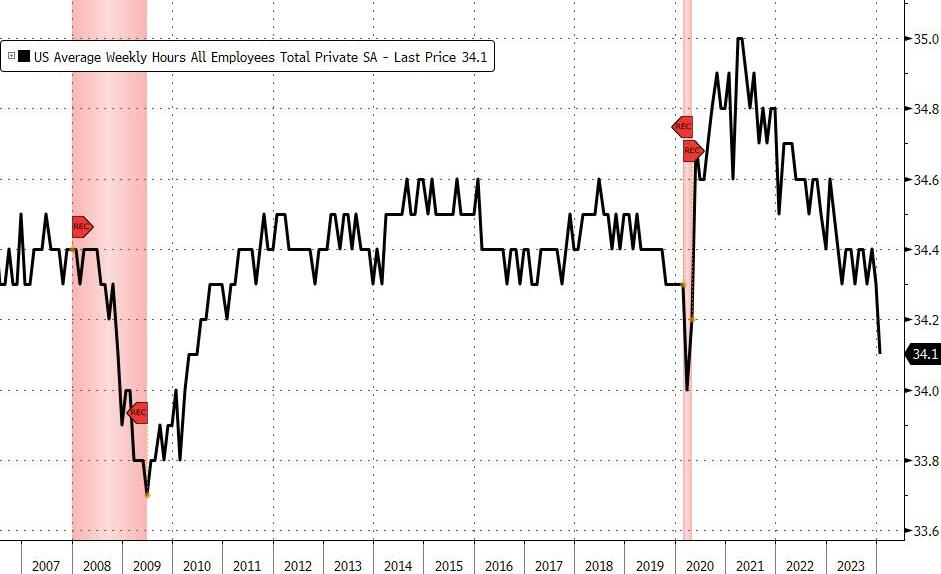

Also telling is that the BLS has sharply slashed the number of estimated hours that everyone was working, from 34.3 to just 34.1. This is a big drop. The last time the workweek was this low was when the economy was shut down during covid. Other than the covid lockdowns, we have to 2010 to find such a short workweek. that was this anemic.

Some economy watchers argue we have been in a rolling recession and we are closer to the end of it than the beginning. Still, if we return to the idea the main factors holding up the American economy are growing debt and government spending we have a problem. It does not help that America's yearly trade deficit just came in at a staggering $773.4 billion. The article in this link, spins this a positive development, after all, it is a huge decrease from the prior year.

Other factors feeding into the economic picture are also fogging reality. For example, a boom in the construction of manufacturing plants started in mid-2021. Last year companies plowed an annualized $220 billion into this sector, which is up by 170% from December 2019. This will have long-term ramifications for the economy as does the fact that this surge in construction will not continue forever.

I would like to end this post by circling back to the issue of jobs. An article that appeared on Zerohedge gives us something to ponder. It called the last jobs report the most ridiculous in recent history. Based on the numbers, it claims that all the job creation in the past four years has gone to foreign-born workers, but there has been zero job-creation for native-born workers since July 2018!

In addition, the Zerohedge article points out that while in January the BLS claims 353K payrolls were added, the Household survey found that the number of actually employed workers dropped by 31K. Those of us who believe economic cycles cannot be eliminated only kicked down the road where they wallop even a bigger punch than if allowed to occur see a lot of reasons to question where the economy is headed.

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

{kind=link}

Subscribe to:

Posts (Atom)