Efforts to justify the most recent market melt-up following the election of Donald Trump are difficult to comprehend if you are one of those already skeptical of this market. A read of the 2009 bestselling book titled, "This Time Is Different" did little to convince me that this time is different. It chronicles eight centuries of financial follies in which financial meltdowns have typically followed real-estate bubbles, rising indebtedness, and gaping deficits. Many of us see a strong similarity between what is happening today and prior financial meltdowns.

A read of the pdf file rather than the 2009 bestselling book titled, "This Time Is Different" delves into the history of economic bubbles. Sadly, periods of rapid credit expansion always end the same way and that is in default. The book written in 2009 by Carmen Reinhart and Kenneth Rogoff makes a solid case that despite many economists being enthralled with our newfangled Modern Monetary Theory, also known as MMT, we should still question just how well debt cycles can be managed.

The failures and meltdowns that are chronicled include state failures, bank crises, currency crashes and destabilizing outburst of inflation. Several interesting points leaped out to me while I was reading the file. One concern was the strong link found that indicated countries experiencing sudden large capital inflows are at a high risk of having a debt crisis. The preliminary evidence over a much broader sweep of history suggests this is often the case. Surges in capital inflows tend to precede external debt crises at the country, regional, and global level since 1800 if not before. Also, periods of high international capital mobility have repeatedly produced international banking crises, this is not only true during the last one hundred years but historically.

|

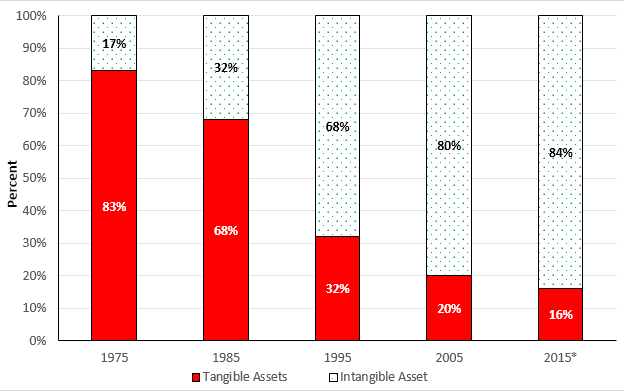

| Note Trend Of Growth In Intangibles |

Efforts to justify the lofty levels of today's markets, especially just a few stocks, are sometimes difficult to comprehend. Part of this is tied to the trend of passive investing coupled with the ability to leverage up and plow into speculative investments. Unfortunately, this has been deemed a good thing because it drives the wealth effect forward and bolsters the notion that pension funds will be able to keep their promises to retirees. Adding to our current market euphoria is the recent bout of financial engineering evident in companies buying back stock. All of these should be enough to give us pause, should markets falter and the wealth effect shift into reverse, the economy would be left in a world of hurt.

Despite mankind's unbridled confidence that the future will be better and our ability to blindly follow our leaders, the elevated markets of today may be placing our future at risk. Even the few people that care about such matters as the overall economy tend to be seek out easy and painless answers even if they are loosely rooted in reality. This again has raised the important issue of whether this time is really different. If not, what happens when the bubble bursts?

(Republishing this article is permitted with reference to Bruce Wilds/AdvancingTime Blog)

No comments:

Post a Comment