|

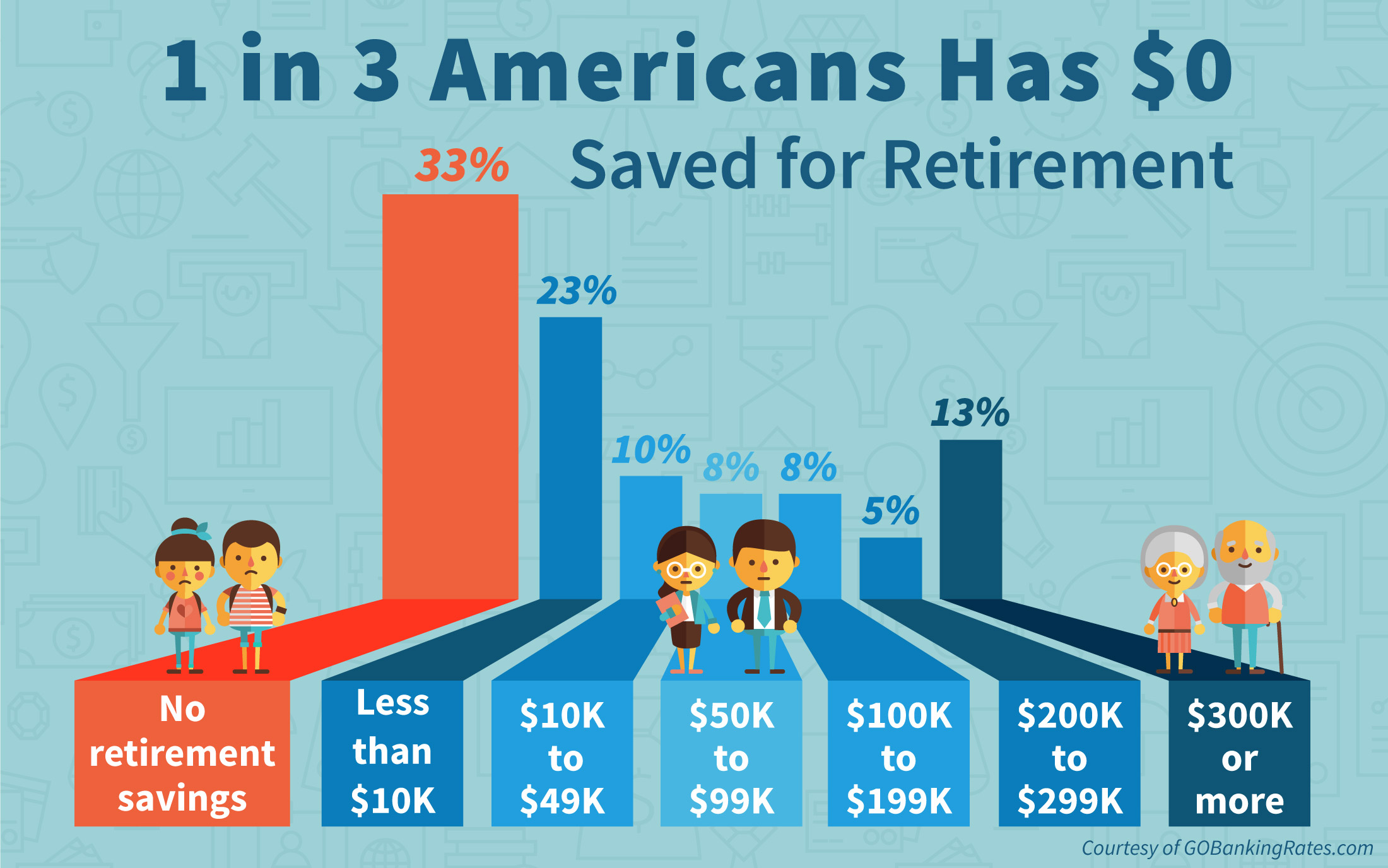

| Most Americans Have Saved Little (click to enlarge) |

The title of this piece referring to the retirement savings resting in US equities is an effort to highlight the danger older investors face. Lower interest rates and a rising market have shifted wealth into stocks and out of savings and other productive investments. This has long-term consequences At one time an American that worked hard and saved a million dollars over their working life could expect to earn enough in interest to live on but not anymore. This has caused far too much wealth and savings to be shifted into equities. In a recent article, the case was made that true price discovery in equities is totally gone. Honest price discovery has fallen victim to the combination of stock-buybacks, and what has become known as the "Plunge Protection Team" appearing to jump in at any sign of any pullback. This leaves the market vulnerable to a huge downward move.

|

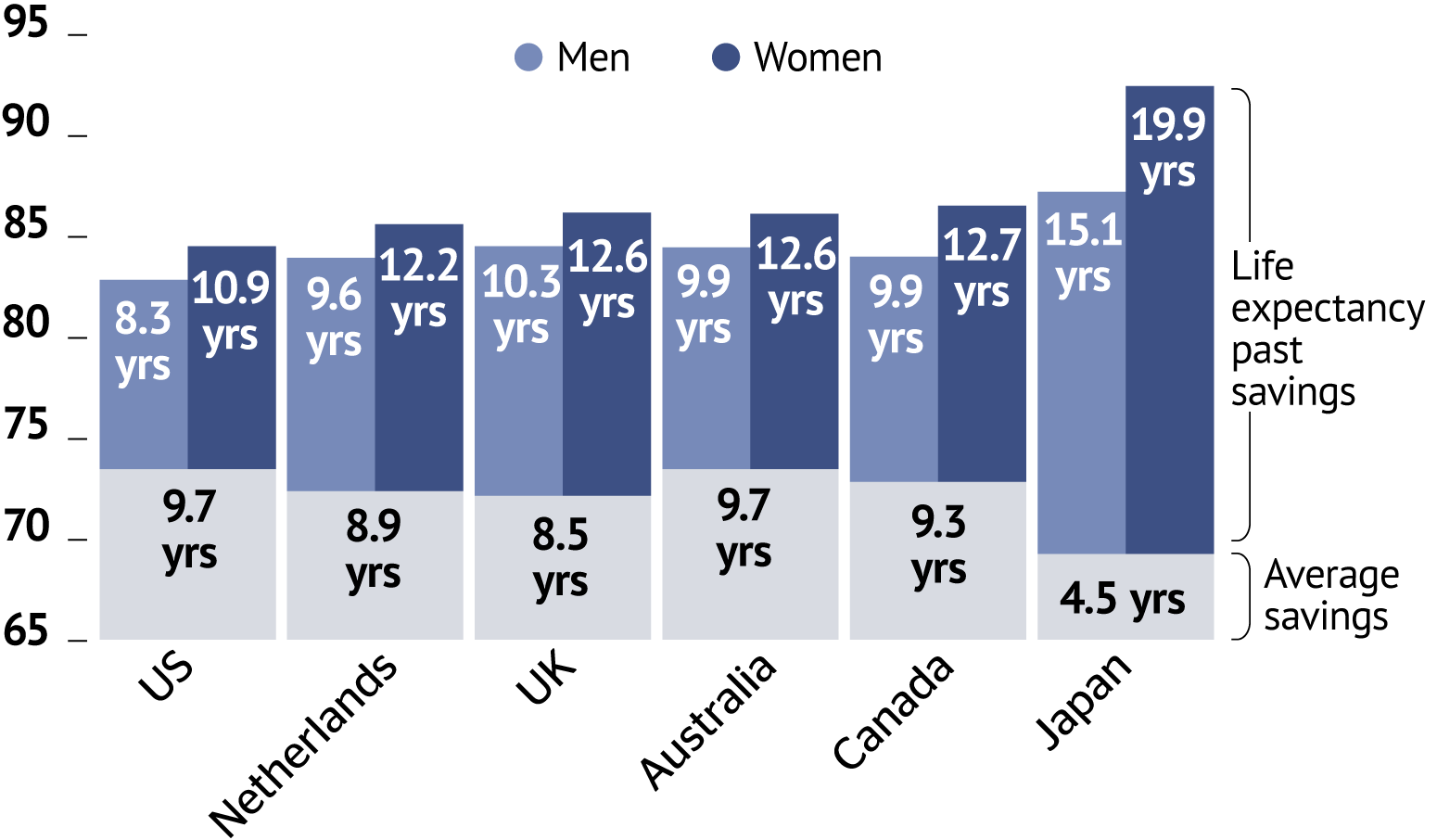

| This Is A Worldwide Problem (click to enlarge) |

Keeping our focus on America, if each new retiree were a raindrop we would be experiencing a downpour. Part of this is because many people are retiring early. For older individuals not earning a high income and not up to their eyeballs in debt much of the incentive to work has vanished. Those not making a great deal in our current low-interest economy often find they do just as well retiring early sometimes even before social security kicks in. As a bonus low-income earners often find Obamacare allows them to replace their expensive healthcare with a far less costly government program. In addition, this means they are often able to qualify for other government programs. Unfortunately, this is putting more pressure on entitlements which increase our huge national deficit.

Simply put, in our current economic environment, it no longer pays to save when inflation is outpacing what you earn on savings. This reality is one of the reasons causing people to retire early and say to hell with work even if it means retirees must cut spending or find new ways to cope. One way they are doing this is reflected in a CBS News report citing Social Security Administration data. It shows the number of retirees who draw Social Security currently living outside the US increased by 40% during the ten years between 2007 and 2017. This translates into more than 413,000 American retirees who collect social security moving out of the country.

The question is how much of this is driven by the financial reality that many baby boomers reaching retirement have not set enough aside for their golden years and this is one way to make ends meet. Just as troubling is that much of their wealth has been placed in paper promises and not tangible assets. These "paper promises" can be unfulfilled and this wealth could vanish if a major economic disruption occurs. While the median retirement savings for people in their mid-60s is around $152,000, the highest of any working generation. It should be noted these savings are not equally shared and many people have saved nothing. Still, most people agree even $152,000 is not enough, especially when factoring in inflation expectations.

The size of the "retirement savings" problem is staggering and getting worse. Figures indicate the size of the world's collective savings gap could be larger than $400 trillion by 2050. That's up from $70 trillion in 2015. The US is forecast to have the biggest retirement savings gap at $137 trillion, followed by China ($119 trillion) and India ($85 trillion). This is difficult to sugarcoat and means a great many older people are about to find themselves in a horrible financial predicament, broke, and too old to do anything about it. This has been cited as a contributor to suicide in older adults. Overall, to say the situation is distressing is an understatement.

Footnote; How much wealth will escape the next large economic crisis is very important because it will set the bar that determines the rate of inflation or deflation in coming years. The article below delves into this issue.

https://brucewilds.blogspot.com/2018/03/how-much-wealth-will-escape-next.html

Hi I am from a non-profit organisation called the Liberalist International Association and we would like to ask if you would like to write an article for us. https://liberalistia.com

ReplyDeleteThis has been "sighted" as a contributor to suicide in older adults? It thought it had been "cited" as a contributor to suicide in older adults

ReplyDeleteThanks, correction has been made.

Delete