|

| BOJ Leads In This Experiment click to enlarge |

Abenomics has consistently missed both its inflation and economic growth targets. Japan has been unable to offset the problem of demographics and productivity with higher debt and money printing. Japan has incentivized malinvestment and government spending has resulted in transferring wealth to unproductive sectors which has zombified the economy. The QQE program was based on three “arrows”; monetary policy, government spending, and structural reforms which never happened because protecting the bureaucratic machine of government always takes priority over what is best for the people.

|

| Shifts From Bigger Players Move Yen - Click To Enlarge |

The yen is part of a somewhat self-defending system of reserve currencies which are considered the most liquid and sound in the global economy. The value between them constantly fluctuates and as one currency falls out of favor investors shift into the other three seeking the least bad choice. As long as savers, investors, and institutions keep their wealth stored within these four currencies and continue the delicate balancing act of avoiding the worse and exiting the most overvalued the system remains relatively stable and will continually readjust partly because it is so self-contained. Each of these currencies has its particular strengths and weaknesses, however, the most vulnerable of the two are probably the Japanese yen and the Euro which is the official currency of the Eurozone, which consists of 19 of the 28 member states of the European Union. A key weakness of the euro is the questionable accountability of its controlling institution.

|

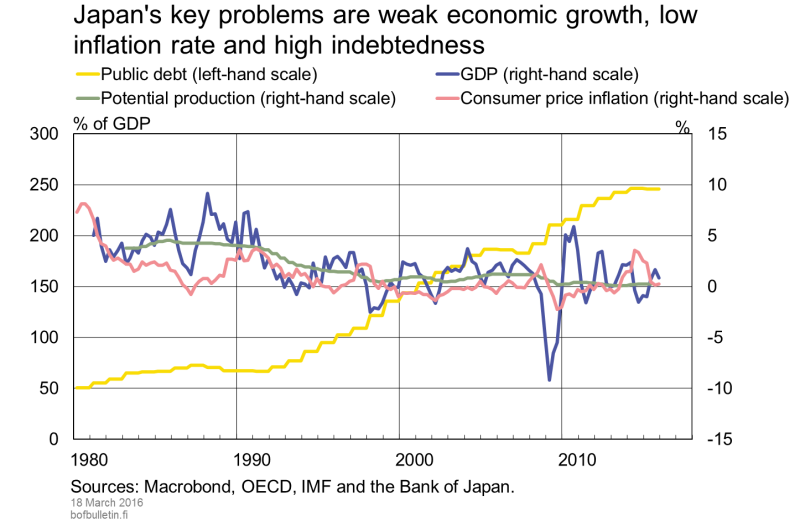

| Weak Growth And Huge Debt click to enlarge |

Demographics paint a bleak picture for Japan which is stuck with an aging and shrinking population that is increasingly expensive for the government to provide for. Adding to its woes the Fukushima nuclear disaster shuttered its nuclear power plants and forced the country to import more expensive energy alternatives. All in all neither monetary nor fiscal policy will adequately solve Japan's problems. Continuing to run fiscal deficits only means that government debt is pushed onward and upward. Simply put, the fundamentals of Japan are lousy. It should be noted that Japan would be sitting in far worse shape if it were not for the wealth currently shifted from America to the small island nation each year. America spends billions each year defending Japan and puts much of this money directly into the economy. Another way America supports Japan is by purchasing many of the goods the country produces. The massive trade deficit America has with Japan feeds large amounts of money into Japan, without this money the massively indebted nation would be in even more trouble.

For years it has been noted that a key strength that Japan holds is its ability to control its own economic fate and that it cannot be held hostage to foreigners because the people and institutions of Japan hold its debt. In the past, we have seen that outside creditors can wield a great deal of sway over a nation that is deeply in debt. It is not uncommon for creditors to squeeze, threaten, and even blackmail a country that owes them a great deal of money. A country can always drive its currency downward, however, supporting it is much more difficult. To drive a currency lower a country only needs to print and sell their currency using it to buy one or more of the other three reserve currencies. It should be noted that in recent years a great deal of the yen's resilience may be contributed to the fact Japan has strong economic ties to China. This bolstered the yen during China's boom years and as growth in China slowed the yen became a conduit to move wealth out of China.

Unlike many other leading economies, Japan has been battling deflation or falling prices for the best part of the past two decades. At some point expect this to change and a new reality to take hold. To support their stock market the BOJ has even gone to buying stock. When investors in Japan's government bonds begin to believe that Abenomics will be successful in bringing back inflation it would be logical for owners of JGB's to move out of low yielding securities and buy foreign bonds or equities. The moment the Japanese stock market fails to rise enough to offset a falling yen and inflation we may see a tsunami of money fleeing Japan. This would constitute the end of the line for those left holding both JGB's and the yen. This has been a long time coming and when this finally occurs and Japan crumbles it will be felt across the world.

Japan with sovereign debt verses private debt:

ReplyDeleteJapanese private savings are immense and a major part of the deflation facing the country. What to do with so much cash.

Discretionary spending is so low compared with the west.

Debt is held in country and carefully monitored unlike the USA with such massive external debt....both private and public.

The ability to hold Foreign capital, property and associated lower costs with diverse manufacturing holds huge reserve for Japan hidden in foreign economies.

Preservation of savings and maintenance of valued assets prevails against consumer based economies.

So how is the value of the currency controlled? QE when being blindsided by a virus that has been a distraction from the norm.

Preceding rhetoric was typical of what has been used to lower the Yen in the past.....

Quantitative Easing aside, the Yen holds so much dominance......beware the common talk....

Thanks for the comment. I addressed some of these issues in my article. The big question is, if many of the Japanese people have massive savings, where are they being held? If it is in cash, any decline in the yen will cause them to seek a safer place to store their wealth. If it is in another part of Japan's internal Ponzi scheme I see danger ahead.

ReplyDelete