|

| Note Where "Buy The Dip" Started (click to enlarge) |

Leading up to this event the stock markets raced upward during the first half of 1987 gaining a whopping 44 percent in just seven months. This, of course, created concerns of an asset bubble, however, few market traders expected the market could unravel so viciously. Prior to US markets opening for trading on Monday morning, stock markets in and around Asia began plunging. In response investors rapidly began to liquidate positions, and the number of sell orders vastly outnumbered willing buyers near previous prices, creating a cascade in stock markets.

Thomas Thrall, a senior professional at the Federal Reserve Bank of

Chicago, who was then a trader at the Chicago Mercantile Exchange

later said, “It felt really scary, people started to understand the

interconnectedness of markets around the globe.”

Without a doubt, several new developments in the market enlarged and exacerbated the losses on Black Monday. Things like international investors becoming more active in US markets and new products from US investment firms, known as “portfolio insurance” had become very popular. These included the use of options and derivatives. A number of structural flaws also fueled the losses. At the time of the crisis, stock, options, and futures markets used different timelines for the clearing and settlements of trades, creating the potential for negative trading account balances and forced liquidations.

That is when, Alan Greenspan, then Federal Reserve chairman, came forward on October 20, 1987, with a statement that would shape traders' actions for decades. Fed Chairman Alan Greenspan said, “The Federal Reserve, consistent with its responsibilities as the Nation's central bank, affirmed today its readiness to serve as a source of liquidity to support the economic and financial system” Prior to this markets were seen as a much riskier venture. The great legacy from the events taking place in 1987 is rooted in the actions and swift response of the Fed, that the central bank would backstop markets. This premise has grown over time.

After Black Monday, regulators overhauled trade-clearing protocols and developed new rules. One of the most important is known as circuit breakers which allow exchanges to halt trading temporarily in instances of exceptionally large price declines. Under these rules, the New York Stock Exchange will temporarily halt trading when the S&P 500 stock index declines 7 percent, 13 percent, and 20 percent. This is done in order to provide investors time to make better informed decisions during periods of high market volatility and reduce the chance of panic. Risk managers also re-calibrated the way they valued options.

Unlike previous financial crises, the Black Monday decline was not associated with a deposit run or any other problem in the banking sector. Still, it was very important because the Fed’s response set a precedent that has over time when coupled with other events massively increased the moral hazard associated with intervention in free markets. Following the rout stock markets quickly recovered a majority of their Black Monday losses. In just two trading sessions, the DJIA gained back 57 percent, of the Black Monday downturn. Because of the Fed action in less than two years, the US stock markets surpassed their pre-crash highs and was not followed by an economic recession.

And now for the grand point of this post, we should not underestimate how the Fed’s response to Black Monday ushered in a new era of investor confidence in the central bank’s ability to control market downturns. The actions by Fed Chairman Greenspan galvanized the mantras "buy the dip" and "don't fight the Fed" and powered them to the top of trading lexicons. It has also been a key factor in allowing the stock market to morph into a much larger symbol of the economy than it merits. This is reflected in how over the decades growth in the financial sector has soared dwarfing that in the real economy.

|

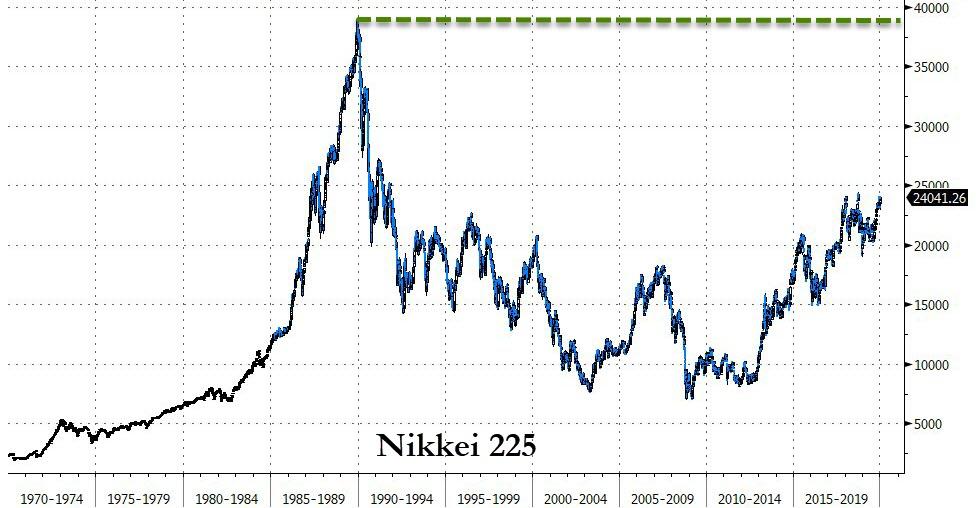

| Decades Of Nikkei Action (click to enlarge) |

Another often overlooked issue is how changes in tax laws over the years have moved more wealth into stocks. These include the often forgotten and seldom mentioned changes many made by the Bush administration following the dotcom bust and 9-11. These factors and money constantly funneled into markets by pension funds and such coupled with soaring central bank liquidity has levitated markets to record high, after record high, despite stagnant fundamentals. It seems the "fear of missing out" and exuberance has caused many investors to become blind to the idea that years of profits can vanish in a blink of the eye.

This should force us to question the utter madness displayed in the widening disconnect between current valuations and underlying fundamentals. It could be argued that because of these actions QE has amplified speculation as investors seeking yield now feel almost invulnerable to future losses. We can cast away all the terms and warnings about "moral hazards" and "slippery slopes," however that does not guarantee they will not return to haunt us. Historically our hubris and arrogance has shined as a beacon illuminating the fact that every time those in high finance declare it is different this time they have been proven wrong.

When 1% of the population has all the wealth can the market actually fall, or do those with little, panic and sell to the 1% waiting to buy at any cost.

ReplyDeleteWill we end up like Europe in the 14 and 15 hundreds, Lords and Ladies and millions of dirt poor serfs or peasants.

Tax the rich now before it is too late!

The current US president has a base of between 29% and 40%. It will not take much to win over a feuding Democratic Party!